[ad_1]

Wirestock

I’m constantly looking into ways to capitalize on the airplane shortage and long-term growth prospects of the aerospace industry. AerCap (AER) has most likely been my best call on that end, and finding similar winners has proven to be challenging. One reason is that there are relatively few lessors of flight equipment and flight-related equipment.

I recently covered FTAI Aviation (FTAI) with a buy rating, but the stock has underperformed the markets. Short-term underperformance, however, is not a major concern of mine, as I view these type of investments opportunities for the mid to longer term. In this report, I will be discussing the prospects of Willis Lease Finance Corporation (NASDAQ:WLFC).

Willis Lease Finance: An Aircraft Leasing Company With Diversification

Willis Lease Finance Corporation, along with its subsidiaries, is a lessor and servicer of commercial aircraft and aircraft engines. The Company operates through two segments: Leasing and Related Operations, and Spare Parts Sales.

The Leasing and Related Operations segment involves acquiring and leasing, primarily pursuant to operating leases, commercial aircraft, aircraft engines and other aircraft equipment and the selective purchase and resale of commercial aircraft engines and other aircraft equipment and other related businesses. The Spare Parts Sales segment involves the purchase and resale of after-market engine parts, whole engines, engine modules and portable aircraft components. The Spare Parts Sales segment also enables the Company to provide end-of-life solutions for surplus aircraft and engines, as well as manage the full lifecycle of its lease assets. Its subsidiaries include WEST Engine Funding LLC, Willis Aeronautical Services, Inc. and Willis Asset Management Limited.

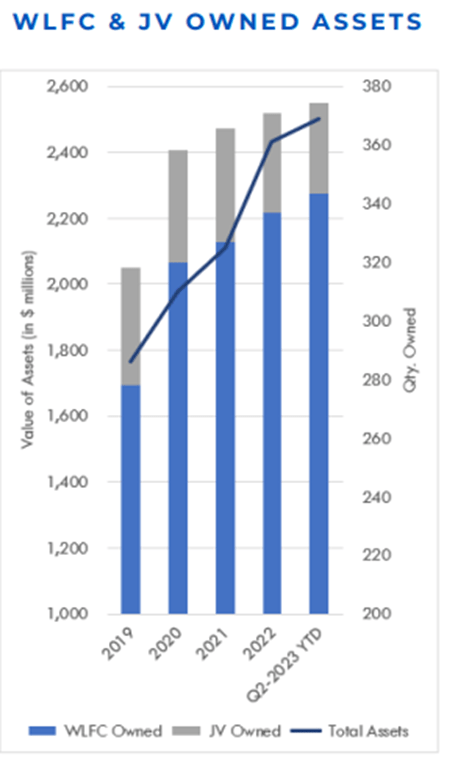

As can be seen from its business segments, Willis Lease Finance is not a pure aircraft lessor as it also generates revenues via spare part sales. Moreover, the company actually should not even be considered a primary aircraft lessor for the simple fact that its portfolio is heavily geared towards engines. The carry value of equipment held for operating lease was $2.2 billion by the end of June 2023, with over 90% exposure to engines and related equipment.

What Are The Growth Drivers For Willis Lease Finance?

Willis Lease Finance

The growth drivers for Willis Lease Finance are the same as for many companies in the aerospace and travel industry: the continued demand for air travel which provides support for growing demand for airplanes and engines. I consider lessors to be superior investment opportunities to airlines due to the tendency of airlines to throw capacity on the market in excess of demand thereby diluting upward pricing power. Aircraft and related equipment, however, are significantly more resistant in the sense that the assets hold value rather well and in the current environment where demand for aircraft and engines outpaces the production plans of Boeing (BA) and Airbus (OTCPK:EADSF) the pricing power for lessors strengthens.

Unfortunately, Willis Lease Finance does not provide an exact breakdown of its engine portfolio but we know it consists of LEAP-1A/B, GEnx, CF34-10E, CFM56-5B/7B, V2500, PW1100G-JM (GTF) and PW1500G (GTF) engines and we do see that the company has been growing its assets base which also drives its revenues higher and should allow it to amortize costs more efficiently.

Willis Lease Finance Revenues Grow Strongly

Willis Lease Finance

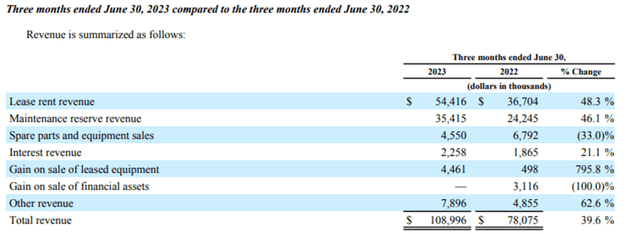

In the second quarter, lease rent revenues grew 48.3% on 10.7% growth in carrying value for its assets held for lease. This figure is an understatement of the actual asset growth based due to continued depreciation, which likely at 3.5 percentage points of growth. So, it would be closer to 14% growth, but it still shows that the lease revenue grew faster than the lease base, indicating better utilization and higher lease rates. Maintenance revenues grew for the same reasons.

Spare parts revenues were down 33%, and while aftermarket sales are still strong, we could see those revenues fluctuate someone as it is not a huge revenue stream for WLFC. Interest revenues were up 21.1%, which is driven by the current interest rate environment, while gains on sale grew 23% due to the sale of two engines compared to 8 engines in the same period last year for lease equipment and notes receivables being sold in the comparable period last year for $3.1 million with no sales in the current quarter. Other revenues which include management fees grew 62.6% bringing the total revenue growth to around 40% and 41% when adjusting for gains on sale and interest revenues.

Expenses climbed from $68.59 million to $89.5 million or 30% driven by a $17.9 million increase in general and administrative expenses including $10 million in personnel costs for bonuses as well as higher project costs and aviation war insurance. Furthermore, on a higher asset base, the depreciation also grew modestly as did the interest expense but those expenses were lower than the booked interest income.

Overall operating income grew little over 100% to $19.4 million indicating a 17.8% margin compared to 11.5% in the comparable period last year while comprehensive income grew from $8.5 million to $13.8 million or 62%. This growth figure was primarily driven down as compared to net income growth due to lower unrealized gains year-on-year.

Willis Lease Finance Corporation

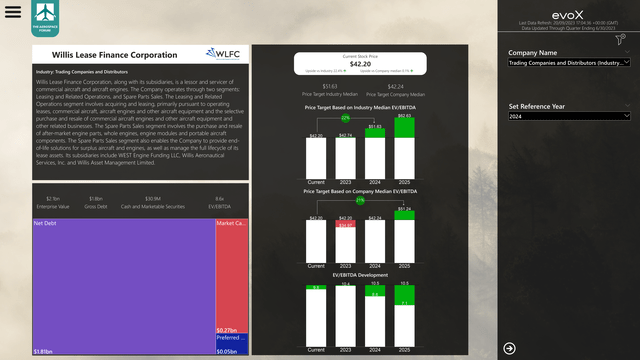

Willis Lease Finance is a relatively small company with a $265 million market cap and receives little analyst coverage. So, there is no quant rating for the stock and no consensus figure available for Wall Street analyst estimates. That makes it even more important for me to inject the numbers for Willis Lease Finance into the evoX Financial Analytics tool to determine a reasonable stock price target. While significant growth is expected, we do see that based on its median EV/EBITDA multiple, the stock is fully valued and even has the 2024 earnings pulled into today’s share price and with multiple expansion in mind, the stock is fully valued with 2023 earnings in mind.

So currently, there is no discount to the stock price and the only reason to buy this is under the assumption that a multiple expansion occurs which would provide 22% upside going forward.

I also value lessors based on the price-to-book ratio, WLFC currently has a ratio of 0.68, while I believe lessors should be trading on a ratio of at least 0.85 which provides 25% upside. So, I would rate the stock a buy at this point.

Conclusion: Willis Lease Finance Is A Company Growing Into Its Valuation

Overall, I am liking the positioning of Willis Lease Finance with regard to its engine leasing exposure, and the stock price also makes it a buy in my view. However, it should also be noted that the company is currently growing its asset base and I would say that drives the upside to the stock, but with $1.8 billion in net debt the company has to realize at least 20% in upside revenue growth per year for it to be worth the investment, as its debt is also growing because the free cash flow is currently not sufficient to cover the growth trajectory that is aspired.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Source link