[ad_1]

PETALING JAYA: Real estate investment trusts (REITs) have remained resilient while the broader equity market suffered heavy losses on concerns of a banking crisis in the United States and Europe.

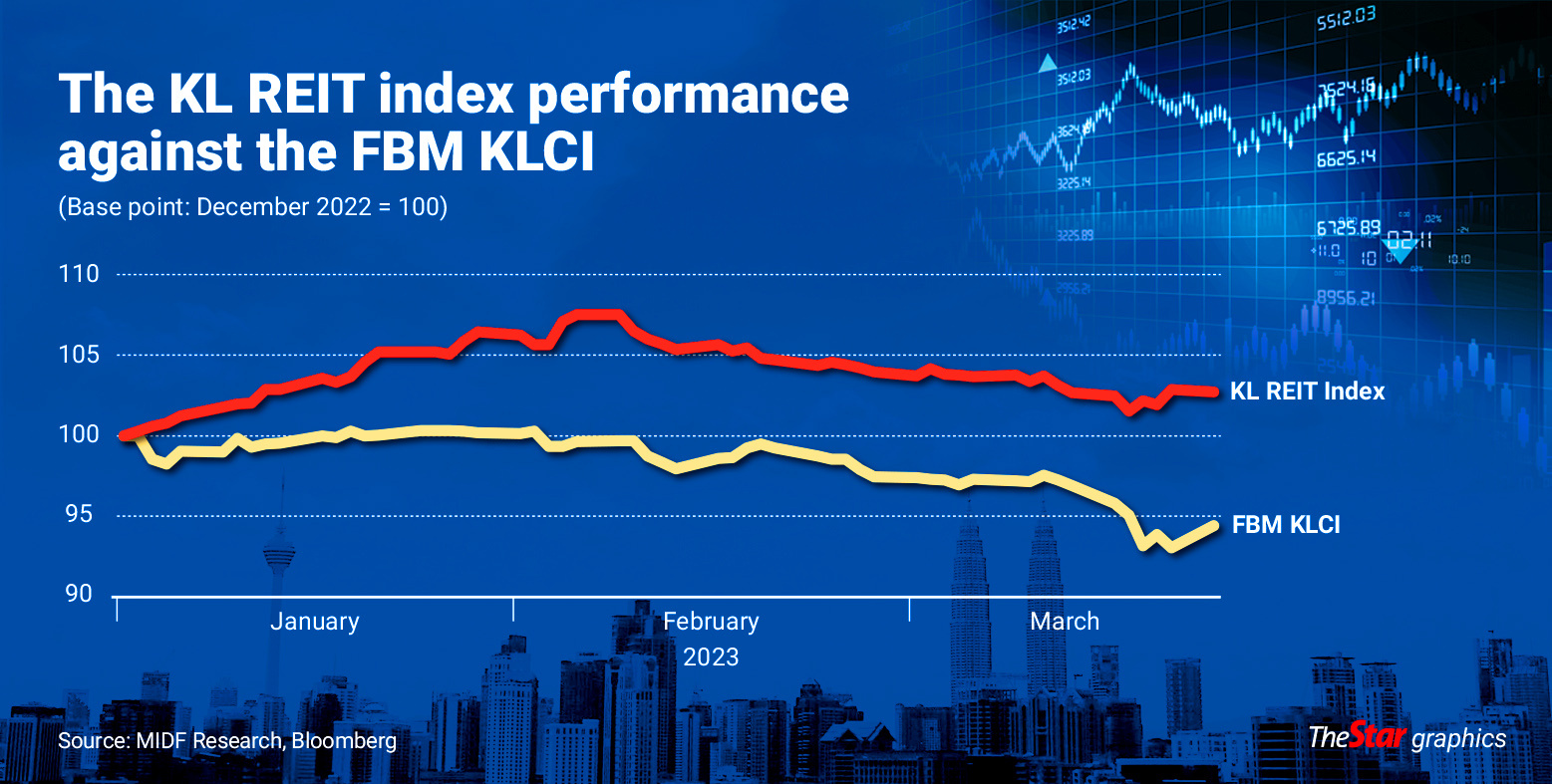

This was evidenced in the decline of the benchmark FBM KLCI of 1.5% within a week after the collapse of Silicon Valley Bank in the United States, while the Bursa Malaysia REIT Index gained a marginal 0.2% during the same period.

MIDF Research said the outperformance of the REIT Index could be due to the defensiveness of the asset class, which provided stable yields.

On a year-to-date basis, the REIT Index also outperformed, with a gain of 2.3% against the FBM KLCI which had lost about 6%.

“We see that investors could be seeking shelter in REITs amid the market uncertainty, as the overall outlook for REITs in Malaysia remains positive, unfazed by the turmoil in overseas markets,” MIDF Research explained.

Reiterating its “positive” stance on the sector, the brokerage named IGB-REIT and Sunway-REIT as its top picks.

“Overall, we see earnings of REITs with exposure to retail and hotels improving further in 2023 due to the recovery in consumer spending at malls and higher tourist arrivals.

“Similarly, industrial REITs, namely, Axis-REIT, is expected to report stable earnings due to solid demand for industrial space,” MIDF Research said.

“In a nutshell, we are positive on the 2023 earnings outlook for REITs, which offer a decent average yield of 5.3%,” it added.

MIDF Research noted that the tapering of the 10-year Malaysian Government Securities (MGS) yield was positive for REITs, as this would widen the spread between the 10-year MGS yield and REIT yields, and increase the attractiveness of REITs for yield-seeking investors.

“The MGS yield tapered down to below 4% in March 2023, as Bank Negara paused interest rate hikes,” it said.

“Looking ahead, we expect the MGS yield to remain below 4%, as our economists expect the central bank to continue to maintain the overnight policy rate (OPR) at 2.75% for the rest of 2023 due to uncertainty in the local and global market conditions,” it said.

In addition, the expected pause in the OPR hike could also ease concerns over rising borrowing costs for REITs, providing relief for REITs with high floating-rate borrowings such as Al-Aqar Healthcare-REIT.

MIDF Research noted that Al-Aqar Healthcare-REIT had 100% Islamic financing on a floating rate, while Sunway-REIT had 68% debt on a floating rate and Pavilion-REIT had 65%.

As such, it said the risk of higher borrowing costs for REITs remained low, implying that earnings growth should remain intact.

[ad_2]

Source link