[ad_1]

sankai

Overview

The OTC Markets Group (OTCQX:OTCM) is a company that operates over-the-counter stock exchanges in the US, markets which investors may have heard colloquially referred to as ‘pink sheets’. In actuality, the pink sheets are only one of the exchanges that the OTC Markets Group offers. The OTCQX market is their most stringent in terms of listing requirements and is the venue where shares of the company itself trade.

These over-the-counter markets work differently than standard stock exchanges and do not require the companies listed therein to report standard filings to the SEC. While there is a wide variance as to each of these company’s respective levels of disclosure beyond that, the lack of that particular requirement stands across the board. This of course creates a different ecosystem of companies than what we find trading on standard stock exchanges.

The OTC Markets Group has a long history and can trace its lineage all the way back to 1913, a time in which it was still called the National Quotation Bureau. It has stood the test of time since then and can presently be considered as the market leader when it comes to over-the-counter stock exchanges. In fact, it doesn’t even have any immediate competitors. It is then a unique destination for a certain class of smaller companies that would generally not be able to list on a standard exchange.

All of this makes OTCM an interesting company to look into at the moment. This is because our current market is seeing the largest companies generating outsized returns, as well as a general lack of breath across equities overall. It would then be reasonable to conclude that this effect has translated into lower investor interest in companies that trade on OTCM’s exchanges, which are in general far smaller and riskier propositions than the greater universe of equities investments. The question then becomes whether OTCM’s business and its share price have been impacted by this, as well as how this determines the best thing to do with its stock going forward.

Fundamentals

A look at OTCM’s revenues in recent quarters shows that the firm had an abrupt revenue decline in Q1, 2022. While revenue had been growing exceptionally quickly prior to that, things suddenly reversed course. The explanation for this happening, as per that quarter’s conference call, was that transaction revenues from customers trading on OTCM’s exchanges decreased significantly.

Seeking Alpha

This appears to confirm an effect of the type that I described earlier. This effect appears to have first hit the firm 5 quarters ago. Perhaps not coincidentally, this was the quarter in which the Federal Reserve began its rate hiking campaign and brought us into our present market regime in earnest.

Yet, revenue growth returned in the next quarter (Q2, 2022) and has been steadily accelerating since. Looking at the conference call transcripts across each of these periods, it turns out that transaction revenue declined in every quarter since Q1 2022 except from the most recent one, Q1 2023.

This means that OTCM’s other revenue channels were able to keep it growing for 3 quarters even as transaction revenues on its exchanges declined for 4 quarters in a row. Revenue growth was then accelerated when transaction revenues picked up 12% in the most recent quarter. As an exchange business, OTCM has proven to be hedged against the immediate effect of lower transactions in its exchanges. It is a set of equity exchanges that proved to be significant enough to see continued interest in its market data even as weaker trading impacted its operations.

The quarter of revenue decline, Q1 2022, had also kicked off a full year of decreased earnings growth for OTCM. While the firm had generally been growing its earnings as briskly as it was its revenues, the most recent year saw this come to a halt. The company nonetheless still managed to grow net income by 1.11% on revenue growth of only 2.14% for 2022.

Seeking Alpha

OTCM’s performance through these recent quarters of turbulence indicate a business that it is resilient and still able to effectively generate profit at the margin. It is interesting to see that the firm did in fact experience a material decline in exchange activity while still being able to continue growing across both the top and bottom line.

Forward View

With its recent fundamental context having been established, we can now consider what’s going to happen with OTCM’s business going forward. Here I think things will continue to reflect what has been going in equities more generally. While we appear to now have one quarter of increasing levels of trading in over-the-counter stocks, that is not enough for a trendline. I am expecting transaction revenues for OTCM to increase again in the next quarter, as well. This is because I think we are at the stage of the market overall where we could start seeing increased breadth again.

Yet, this effect could very well be cut short amidst bearish volatility in the near-term. Given that there are still material uncertainties around the macroeconomic environment as well as consumer spending, we could see tepid earnings growth or even earnings decline in the near future. This would quite likely drive down stock prices as a result. In turn, this would further hamper OTCM’s transaction volumes as the flight to safety and market preference for the largest firms persists.

However, we have already seen that OTCM can continue growing even if downward pressure on transaction volumes were to occur. This business is situated well enough to continue growing revenues, and quite likely profits, in either case. This likely stems from the fact that it is a unique player that oversees a unique niche. There is no competing set of over-the-counter exchanges, with these market leaders all overseen by OTCM.

All of this creates the potential for upside in the near to medium term, while also protecting the firm’s downside as to its growth profile. It also creates an excellent strategic position for the firm over the long-term. This is something that appears well-known by the market and is and well reflected in its share price. OTCM trades at a 141.4% premium to the financial sector on a trailing basis and 135.8% on a forward basis. This is a premium financial stock.

Seeking Alpha

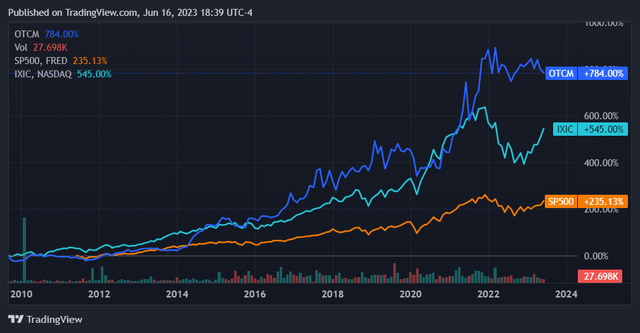

We can see how this premium valuation came to be based on the stock’s trading history. Since 2010 we can see that OTCM has outperformed both the NASDAQ Composite and the S&P500 by a good margin. More specifically, we can see that the stock started a new run of outpacing the NASDAQ Composite (IXIC) throughout 2022 and has stagnated since. Given its excellent growth during that time, it makes sense that the stock was getting bought up, and it also makes sense that things have become less exciting now that growth has moderated. The firm has not captured recent market optimism in NASDAQ names recently, reflecting the lack of breadth that we’ve seen in the market.

Seeking Alpha

This chart means that OTCM shares should start seeing momentum again upon returning to high rates of revenue growth. This will be achieved by growth in its transaction revenues. Investors betting on this stock are really betting on a renewal in trading volume for the microcap equities that are listed on OTCM’s exchanges. As of last quarter, we had this begin to happen anew, but it is unclear if it will persist amidst greater uncertainty.

Conclusion

To reiterate my logic around OTCM stock, I think that it should start seeing upward momentum in its shares as revenue growth picks back up to health double-digit levels. Given what has been playing out over the last 5 quarters, I think it is clear that this will happen from increased transaction revenues in particular. In turn, these increased transaction revenues will stem from increased transaction volumes in the shares of companies listed on its exchanges. Furthermore, this will occur as breadth returns to the market, which will occur as uncertainty decreases.

This can play out in one of two ways in the near-term. Either we have a soft landing, and we see smooth sailing for the economy as well as equities, which should see renewed investor interest in smaller names (increasing breadth). The alternative is that we have a downward period through which the current market regime persists. This will in turn continue our current market regime until a new market begins. The timing and type of which would be unclear.

My take is that OTCM is well-positioned in either case for investors buying for the long-term. We have already seen that it has robust revenues and earnings, even as the current market has weighed on its prospects. It is slated to persist and even grow slowly if the overall environment remains uncertain and challenging. An upswing in the environment should see it return to growth levels that we saw prior to 5 quarters ago, which were exceptional. The company should also be able to readily convert these revenues in earnings, as it has been. That creates a limited downside case as well as a healthy upside case. Overall, I think OTCM should continue to be positioned well due to its unique nature and that its stock is a buy for a 5-10 year horizon.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Source link