[ad_1]

National Insurance payments are being cut for millions of employees from Saturday.

However, other changes mean the amount of tax people pay overall is rising to record levels.

How is National Insurance changing for employees?

From 6 January, 27 million employees will pay 10% on earnings between £12,571 and £50,270. This replaces the previous National Insurance (NI) rate of 12%.

For someone on an average full-time wage of £35,000 the cut is worth about £450 a year, according to the Institute for Fiscal Studies think tank.

Type your annual salary in the calculator below to work out how much this change will benefit you.

Your device may not support this calculator

NI on income and profits above £50,270 will remain at 2%.

NI is not paid by people over state pension age, even if they are working. Eligibility for some benefits, including the state pension, depends on the amount of NI payments you have made.

How is National Insurance changing for the self-employed?

There are also two changes to NI coming for the UK’s two million self-employed people.

From 6 April 2024, they will pay 8% on profits between £12,571 and £50,270, down from 9%. The government says this will be worth £350 a year for self-employed people earning £28,200.

From the same date, self-employed people will no longer pay a separate category of NI called Class 2 contributions. The government says this will save the average self-employed person £192 a year.

What is happening to National Insurance thresholds?

NI is the second biggest source of money for the government. It applies across the UK.

It has frozen the level of income at which you start paying NI (the threshold) at £12,570 until 2028.

It means that as wages rise, more people will have to pay NI.

Why are millions paying more income tax?

As wages rise, more people will also have to start paying income tax and more people will have to pay higher rates.

This is because, as with NI, thresholds are being frozen until 2028.

The tax-free personal allowance will remain at £12,570. (Most taxpayers do not pay any tax on income below this level).

The point at which higher tax rates take effect will also not be increased.

The freezes will create 3.2 million extra taxpayers by 2028, and 2.6 million more people will pay higher rates of tax. That’s according to the Office for Budget Responsibility (OBR), which independently assesses the government’s economic plans.

It expects the policy to raise £25.5bn more a year by 2027-28 than if the NI and income tax thresholds had gone up in line with inflation.

According to the IFS, by 2027-28 an employee earning £35,000 “will be paying about £440 a year more in direct tax overall as a result of all the changes to income tax and NICs since 2021”.

What are the current rates of income tax?

You pay income tax to the government on earnings from employment and profits from self-employment.

Income tax is also paid on some benefits and pensions, income from renting out property, and returns from savings and investments above certain limits.

These rates apply in England, Wales and Northern Ireland:

The basic rate of income tax is 20% and is paid on earnings between £12,571 and £50,270 during the tax year, which runs from 6 April to 5 April the following year.

The higher rate of income tax is 40%, and is paid on earnings between £50,271 and £125,140.

Once you earn more than £100,000 a year, you also start losing your tax-free personal allowance. This means you have to pay income tax of 40% on some of the first £12,570 of your earnings.

You lose £1 of your personal allowance for every £2 that your income goes above £100,000. So if you earn more than £125,140 a year, you no longer get any tax-free personal allowance.

The additional rate of income tax is 45%, and is paid on all earnings above £125,140 a year.

How is tax different in Scotland?

Some income tax rates are different in Scotland.

From April 2023 the rates are:

- Tax-free personal allowance: £12,570 (reduced by £1 for every £2 earned above £100,000)

- Starter rate of 19%: £12,571 to £14,732

- Scottish basic rate of 20%: £14,733 to £25,688

- Intermediate rate of 21%: £25,689 to £43,662

- Higher rate of 42%: £43,663 to £125,140

- Top rate of 47%: above £125,140

In December, the Scottish government announced a new “advanced” rate of 45% for those earning between £75,000 and £125,140. The top rate of tax will also increase to 48%.

From April 2024, the new rates will be:

- Tax-free personal allowance: £12,570 (reduced by £1 for every £2 earned above £100,000)

- Starter rate of 19%: £12,571 to £14,876

- Scottish basic rate of 20%: £14,877 to £26,561

- Intermediate rate of 21%: £26,562 to £43,662

- Higher rate of 42%: £43,663 to £75,000

- Advanced rate of 45%: £75,001 to £125,140

- Top rate of 48%: above £125,140

The Scottish government estimates that 114,000 people will pay the new advanced tax rate and a further 40,000 the top rate.

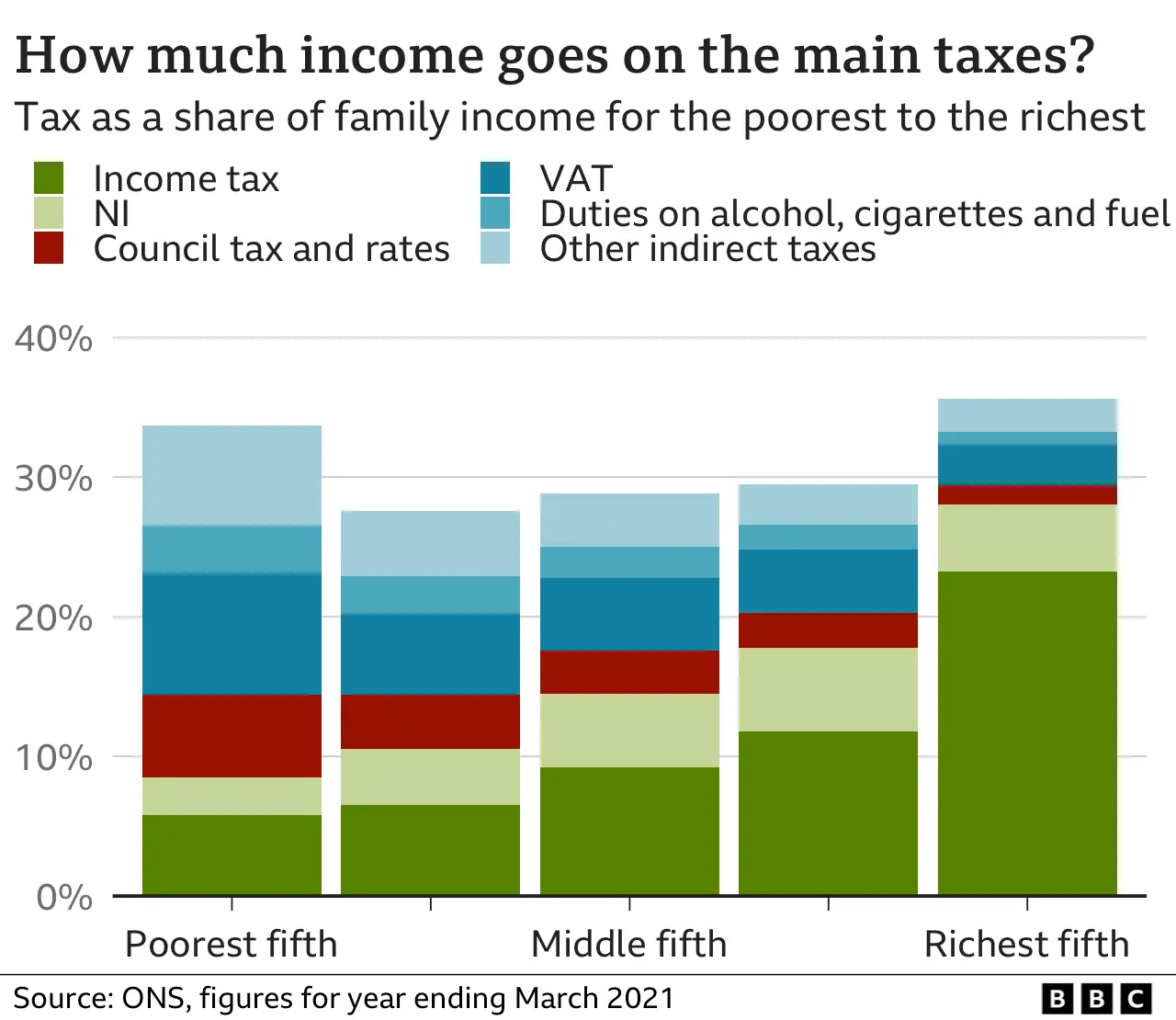

Who pays most in income tax?

For most families, income tax is the single biggest tax.

But poorer households tend to pay more through indirect taxes on the money they spend.

For the poorest fifth of households, VAT is the biggest single tax paid.

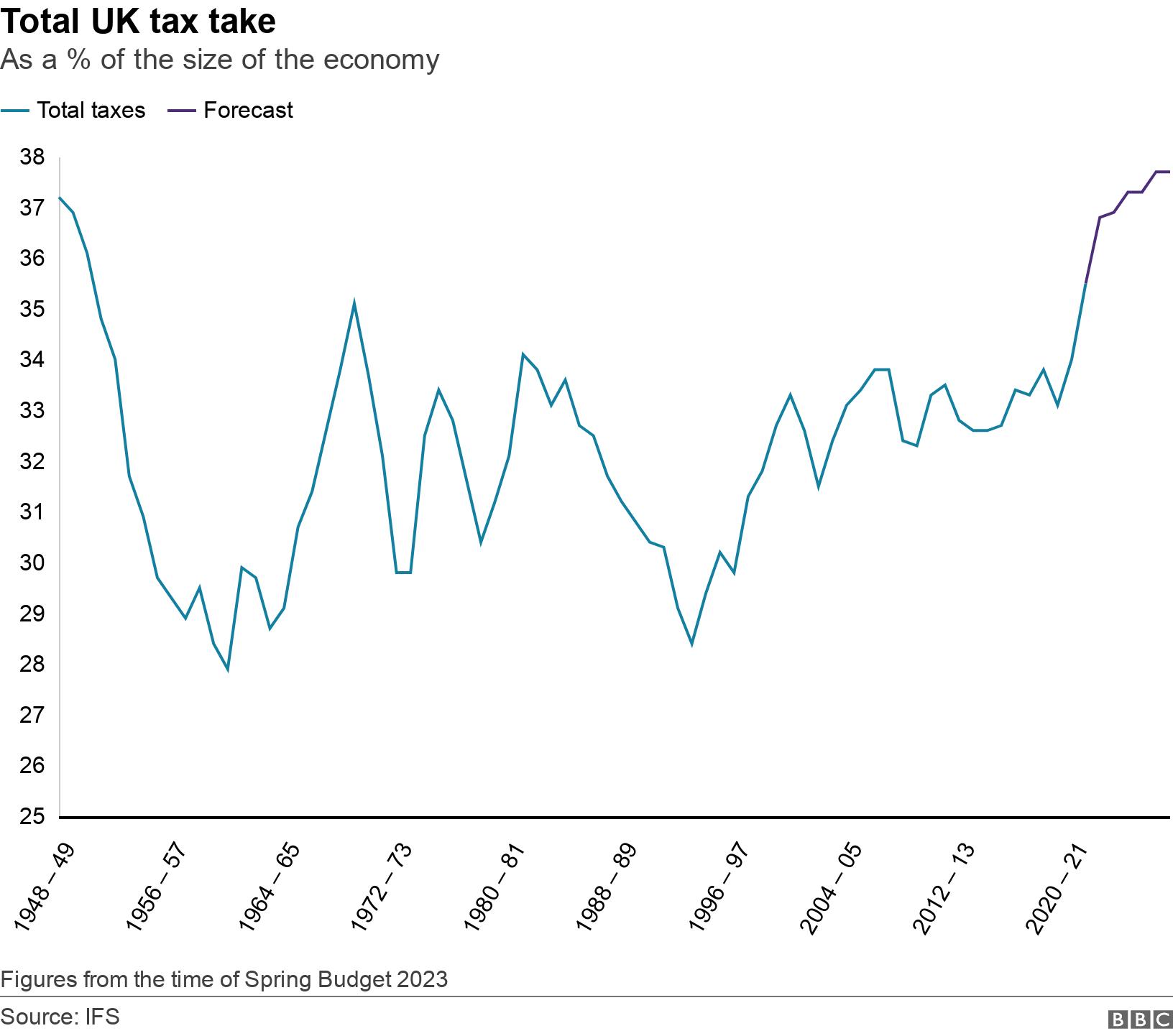

How high are UK taxes historically?

One way of measuring how high overall taxes are is to compare them with the size of the economy.

At the time of the Autumn Statement, the OBR said they would rise “in each of the next five years to a post-war high of 38% of GDP”.

How do UK taxes compare with other countries?

If you look at the amount of tax raised as a proportion of the size of the economy in 2021 – the most recent year for which international comparisons can be made – the figure was 33.5%.

That puts the UK right in the middle of the G7 group of big economies.

France, Italy and Germany tax more, Canada, Japan and the US tax less.

[ad_2]

Source link