[ad_1]

A quiet overnight session despite the plethora of earnings reports.

Todays podcast

- Little change in equities or rates, USD weaker (DXY -0.4%)

- Fed speak points to a May hike, Bullard wants two more on top

- UK wages comes in hot, markets lift BoE pricing to 90% for May

- RBA Minutes yesterday shows May is very ‘live’, Q1 CPI key

- Coming up: UK CPI, ECB’s Lane, US Beige Book, Earnings

“Some like it hot and some sweat when the heat is on; Some feel the heat and decide that they can’t go on” Power Station, 1985

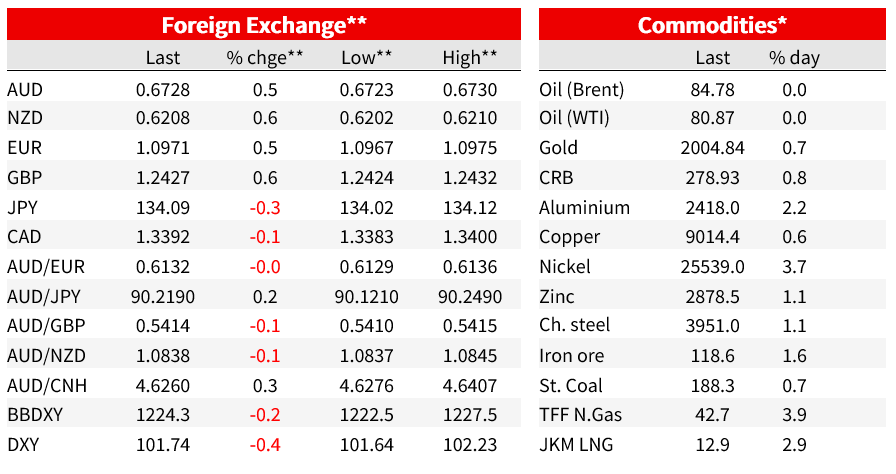

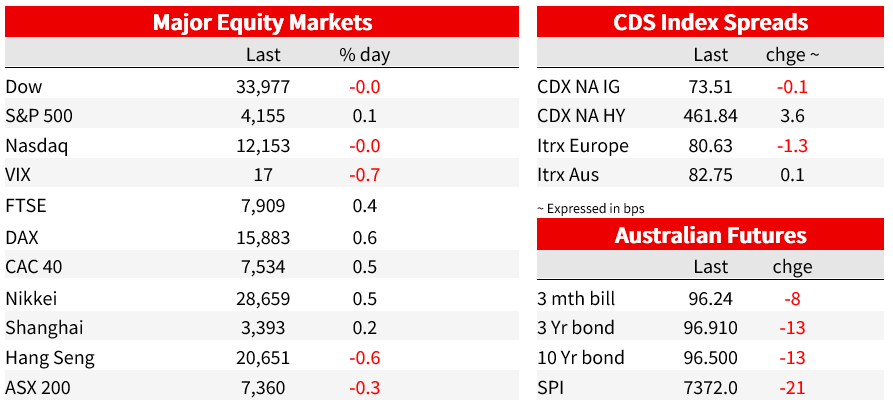

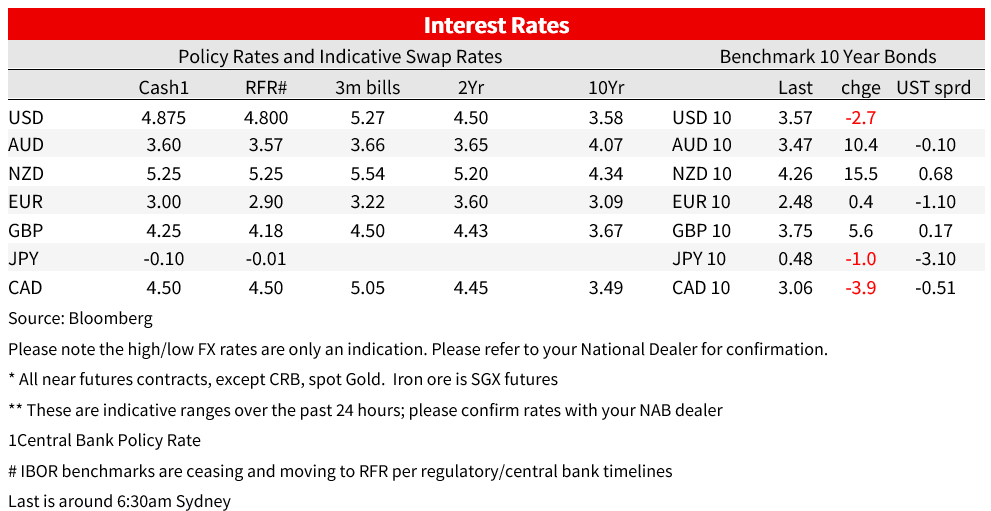

A quiet overnight session despite the plethora of earnings reports. The S&P500 closed up 0.1%, retracing the initial 0.4% rise seen at the open as analysts scrutinised headline earnings reports. BofA (+0.6%) and Goldmans (-1.7%) both reported with BofA beating and Goldmans disappointing on revenue. Importantly for the outlook there was no evidence of credit deterioration, though BofA is still forecasting a mild US recession. It is clear from the banks so far that fears of a banking crisis have receded, and instead the focus is turning to what extent banks tighten up lending standards. Yields were little moved with no top tier data. The US 10yr yield was -2.7bps to 3.57% and the 2yr was flat at 4.20%. The 3m T-Bill yield though did rise to 9.6bps to 5.10%, its highest since 2007. Fed speak by Bostic and Bullard (both non-voters) again pointed to a May hike, while Bullard wanted another two on top of that to 5.50-5.75%. Across the pond UK wages data came in hot (5.9% y/y vs. 5.1% expected) with BoE pricing lifting in its wake with May now 90% priced and a peak of 4.78%, up from 79% and 4.69% on Monday. UK yields also rose with the 10yr up 5.6bps to 3.75%.

First to US Fed speak. Although not market moving, it does reinforce the base case of the Fed lifting rates again in May, with little chance at this stage of sizeable rate cuts in H2 2023. The Fed’s Bostic (non-voter) noted that “one more move should be enough for us to then take a step back and see how our policy is flowing through the economy, to understand the extent to which inflation is returning back to our target ”. As for the pricing of cuts, Bostic said inflation was still running too strong to consider cuts and that inflation isn’t going to moderate as quickly as some of the markets do (see CNBC: Bostic Interview). Meanwhile Bullard (non-voter) was more hawkish, wanting three more hikes to 5.50-5.75%. Bullard noted that he doesn’t see a recession given “the labor market just seems very, very strong”. Bullard downplayed the recession forecasts coming from models which in his words “…put too much weight on the idea that interest rates went up quickly ” and given little weight to labour market strength and accumulated savings during the pandemic (see Reuters: Bullard Interview). On accumulated pandemic savings, BofA noted its consumer deposits were still 42.5% higher than pre-pandemic.

Turning to the profit reporting season, the KBW bank index was up 0.2% and regional banks underperformed with KRE -2.2%. BofA (+0.6%) beat expectations, while Goldmans (-1.7%) missed on revenues. BofA earnings were 94 cents per share vs. 82 cents expected, while revenue was $26.39bn vs. $25.13bn expected. Goldmans meanwhile missed on revenue at $12.22bn vs. $12.79bn expected, with a consumer loan hit and weaker-than-expected bond trading and asset and wealth management results. As for outlook, BofA CEO Moynihan said he sees only a slight recession hitting the consumers remain in solid shape: “Everything points to a relatively mild recession given the amount of stimulus that was paid to people and the money they have left over ”. The two clear implications from the profit reporting season from banks is that there is no evidence of credit deterioration, and fears of a banking crisis are receding. Also reporting on Monday, but after the close was JB Hunt Transport, which noted average load per trailer for contractors were down 24% y/y – CEO Shelley said “simply stated, we’re in a freight recession”.

Across the pond UK labour market data came in hot. Average Weekly Earnings excluding bonuses were 5.9% y/y vs. 5.1% expected and the prior month was also revised up to 5.9%. Including bonus it was 6.6% vs. 6.2% expected. Given policy makers had expecting a cooling in pay growth, the data suggests the BoE needs to do more. Employment growth was also strong at 169k vs. 50k expected, while the unemployment rate ticked up one tenth higher to 3.8%. BoE pricing now has a 90% chance of a 25bp rate hike in May (up from a 79% chance on Monday), with another by August and a good chance of another by September (in total 61.0bps are priced, bringing terminal to 4.78% compared to 4.69% yesterday). Elsewhere across the channel the German ZEW Expectations moderated to 4.1 vs. 15.6 expected. Canadian CPI was broadly as expected with the trimmed mean at 4.4% y/y. The BoC Governor said he couldn’t rule out further hikes in Parliament, though markets price little risk of this. ECB President Lagarde also made one interesting remark, noting if geopolitical fractures re-define global trade routes then CPI would rise 5% in the short term and 1% in the long-run – something to look for given elevated geopolitical tensions.

In APAC yesterday Chinese activity data showed GDP rebounded more quickly than expected. Q1 GDP growth beat by two tenths at 2.2% q/q vs. 2.0% expected. Strength was seen by the consumer with retail sales 10.6% y/y vs. 7.5% expected. Although industrial indicators were a little softer than expected (3.0% y/y vs. 3.5% consensus), stimulus measures and the pickup in credit should underpin industrial/investment growth. The Chinese data beat did help support risk sentiment in APAC and helped lift the AUD along with the RBA Minutes for April (more below). the key move in currency markets has been modest broad-based weakness in the USD, reversing some of the prior day’s strength. Since this time yesterday, the key majors are up around 0.4-0.6%, with JPY and CAD slightly lagging. The NZD is currently just over 0.62, after trading up to about 0.6225 overnight. AUD is trading around 0.6730.

Finally the RBA April Minutes suggested the May RBA meeting is very live. Although the RBA did end up pausing in April, the merits of a 25bp hike was debated. Importantly, the decision to pause in April was not de-facto pre-commitment to pause for several. Clearly the Q1 CPI on 26 April and staff forecasts will be important for May. The debate on 0 vs. 25 within the Minutes highlights that a tightening bias remains and that the RBA is testing the limits of its own willingness to tolerate above-target inflation. Dr Lowe noted in his recent speech, the RBA is aiming to get inflation back to around 3% by mid-2025, deliberately taking a different approach to some other central banks by preferring to try and retain as much of the gains in the labour market as possible, against getting inflation back to target sooner. However, the Minutes also note “…that it would be inconsistent with the Board’s mandate for it to tolerate a slower return to target” than what was contained in the February SoMP forecasts.

Coming up:

- EZ: Final-CPIs and ECB’s Lane: The final versions for the March CPIs are out with no revision expected. Recall headline was 6.9^ y/y and core was 5.7% y/y. ECB chief economist Lane is also giving a keynote speech at Enterprise Ireland Summit in Dublin.

- UK: CPI & BoE’s Mann: Core CPI is expected to remain elevated at 6.0% y/y, while headline is expected to fall back on base effects with consensus at 9.8% y/y from 10.4%.

- US: Beige Book, Fed’s Williams & Earnings: The Fed’s Beige Book is out, while the Fed’s Williams speaks at the Money Marketeers of New York University. Elsewhere the earnings season continues with notable names including Morgan Stanley, IBM and Tesla.

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

[ad_2]

Source link