[ad_1]

Todays podcast Soft US PPI helps drive a risk-on rally Adds to views the US Fed is almost done USD […]

Todays podcast

- Soft US PPI helps drive a risk-on rally

- Adds to views the US Fed is almost done

- USD falls, and AUD and NZD outperform

- Yields mixed, equities up ahead of earnings

- Coming up: US Retail Sales, US Bank Earnings

“Love is in the air, everywhere I look around; Love is in the air, every sight and every sound; And I don’t know if I’m being foolish; Don’t know if I’m being wise; But it’s something that I must believe in; And it’s there when I look in your eyes”, John Paul Young, 1977

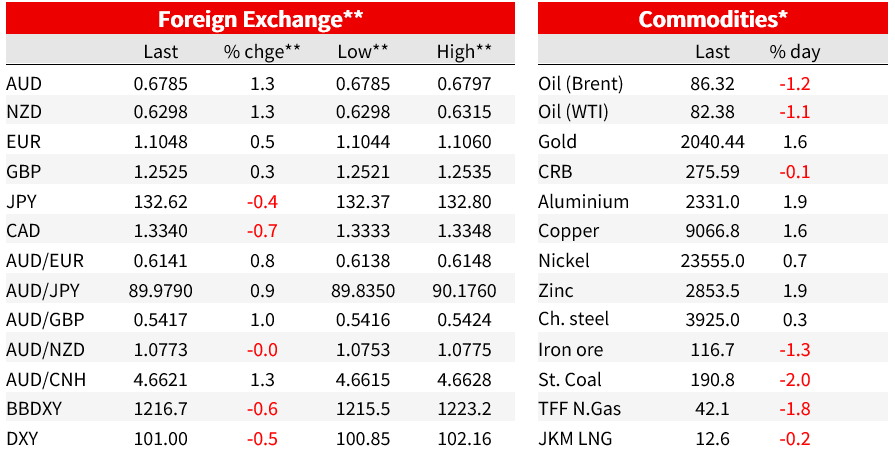

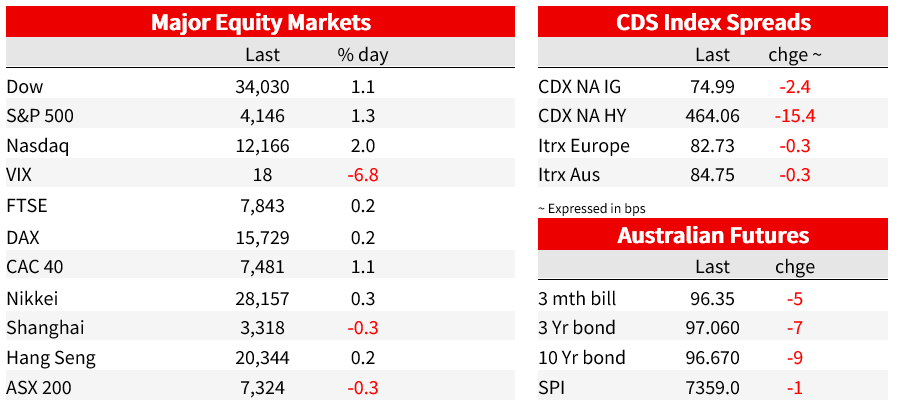

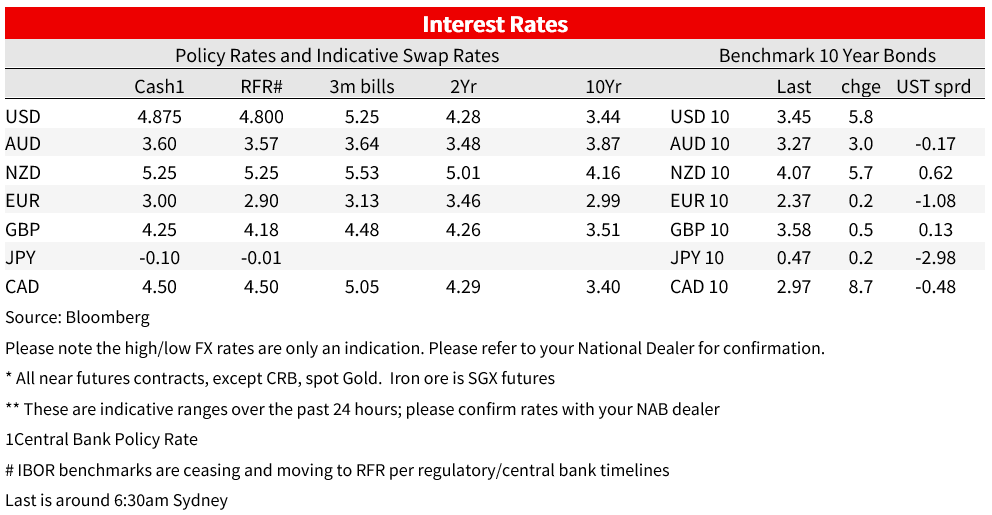

More signs of easing US inflationary pressures has added to views that the US Fed is almost done with its hike cycle. Headline March PPI was -0.5% vs. 0.0% expected and is the largest monthly decrease since April 2020, while Core PPI was also soft at -0.1% m/m vs. 0.2% (albeit with a two tenth upward revision to the prior month). While US Fed rate hike expectations held steady for May at 69%, the curve continues with its aggressive pricing of cuts with 69bps worth of cuts priced in H2 2023. Yields were mixed with the curve steepening: the 2yr held broadly steady at 3.96%, while the 10yr rose 4.9bps to 3.45%. The implied inflation breakeven was broadly steady at 2.29% with most of the move reflected in the 10yr TIP yield at 1.15%. Equities in contrast had a much sharper reaction. The S&P500 closed +1.3% along with the NASDAQ +2.0%, moves likely exacerbated by positioning ahead of the earnings season. Key US banks report tonight (incl. Wells Fargo, JPMorgan and Citigroup). The USD fell with DXY -0.5%. Outperforming were the AUD (+1.3%) and NZD (+1.3%) buoyed by risk sentiment, and for the AUD partly by yesterday’s steller jobs figures.

First the PPI. There were more signs of cooling inflationary pressure in the US in the PPI overnight. Headline PPI was -0.5% m/m vs. 0.0% expected with the decline being the largest monthly decrease since April 2020, while Core PPI was also soft at -0.1% m/m vs. 0.2% expected (albeit the prior month was revised up by two tenths). Annual Core PPI is now running at 3.4% y/y. As economic activity slows, the probability that firms pass on easing cost pressures increases and thus softer Core CPI/PCE inflation is looking more likely. Not getting much airplay yesterday, but worth noting in the context of easing inflationary pressures, is the Cleveland Fed’s Trimmed Mean CPI rose just 0.2% m/m in March, a substantial deceleration from the 0.5-0.6% pace seen since December 2022. That same substantial easing in inflationary pressures was also seen in the ISM last week. Also out overnight was Jobless Claims which rose broadly as expected to 239k from 228k (consensus 235k), with some signs perhaps that recent layoffs in the tech sector are showing up with a large rise in claims coming California.

Also adding to the hopes of cooling global inflationary pressure is China. The trade figures for March were much better than expected and showed a surge in exports of 14.8% y/y, well above the consensus of -7.1%. The scale of the increase suggests supply chains have rapidly improved (which your scribe has noted from clients over recent months), but China is also expanding market share in Asia and Europe – Russia in particular. Whether export growth can be sustained given global headwinds is of course uncertain and the WSJ notes last week, China’s new Premier Li Qiang called for more support for manufacturers selling to developed economies, as well as deepening ties in the neighbouring markets. As for import growth that was also stronger than expected at -1.4% y/y vs. -6.4% expected, a solid indicator of domestic demand rebounding, while the headline trade balance increased to $88.2bn from $16.8bn

In FX, the USD was weaker across the board with the DXY -0.5%. As noted above the AUD and NZD both outperformed, up around 1.3%. Other major pairs were mostly stronger with EUR +0.5% and trading at its highest level in over a year, up through 1.1050. USD/JPY was -0.4%. Of the majors, GBP has risen the least by 0.3%, even if trading at a fresh 10-month high through 1.2530. While not market moving, UK Monthly GDP for February disappointed at 0.0% m/m vs. 0.1%, though the prior month was revised up a tenth to 0.4%. Strike action during February likely weighed on activity. Meanwhile the BoE Chief Economist remained hawkish, noting that the UK could experience a “positive demand shock” as rock-bottom unemployment leaves workers with more to spend, and that “ right now, I am worried about inflation being too high because we need to get back to target,” “But in doing that, we need to recognize there is scope to do too much as well as too little.”. Markets continue to price around a 80% chance of a BoE May rate hike, and an 80% chance of another hike by August.

Finally in Australia, employment grew 53.0k m/m in March, more than double the consensus of 20k. The unemployment rate held steady at 3.5%, where it has been since July 2022 and it remains around its lowest levels since the 1970s. The interesting feature of the numbers was a sharp recovery in population growth with the population aged 15 years plus increasing by 2.3% over the past year, equivalent to an increase in the population of 481.5k. The shortfall in population relative to the pre-pandemic trend is shrinking, with around 36% of the gap between a pre-pandemic population trend having been made up since December 2021 (the gap now stands at 287.9k vs. a peak gap of 452.8k in December 2021). For the RBA, the data shows the labour market is still tight, but not necessarily tighter than what the RBA had pencilled in their February SoMP which had an unemployment rate of 3.6% in the June quarter. We expect Q1 CPI data on 26 April will be the primary determinant of whether the RBA hikes again in May.

Coming up:

- NZ: Manufacturing PMI: not market moving and no consensus available, prior month was 52.0.

- EZ: ECB speak: the ECB’s Nagel speaks in Washington

- US: Retail Sales, Uni Michigan Sentiment, & Bank Earnings: retail sales for March are expected to fall with the core control group -0.5% m/m. Bank card data suggests downside risks. Fed speak continues with the Fed’s Waller discussing the economic outlook with Q&A. Earnings season also kicks off in earnest with Wells Fargo, JPMorgan and Citigroup all reporting with focus on lending standards and credit conditions.

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

[ad_2]

Source link