[ad_1]

After months of protests, violent clashes with police and a government accused of betraying the constitution, France’s President Emmanuel Macron has made the most dramatic changes to the nation’s pension system in a generation.

Until the recent reforms, French workers were legally allowed to retire at 62, and while that does not guarantee a full pension unless they have worked and contributed for enough time, Macron has managed to increase that age to 64.

Historically, pensions have been a major political flashpoint in France, and this current showdown between the government and workers is as volatile as ever.

“Every country has its sacred cows”, Nicholas Barr, professor at the London School of Economics European Institute, told Al Jazeera. “In France, altering the pension age is very much a sacred cow.

“To give you other examples of sacred cows, in the US it’s the mere mention of any public involvement in healthcare, when you get instant shouts of ‘communism’ and ‘socialism’; in Britain you bring in the slightest hint of private delivery in the National Health Service and you promptly get cries of betraying all the principles of the NHS.

“And in France the equivalent, the third rail, is pension age. And while you can recognise that the issue is a third rail, the idea that the pension age can be kept at 62 is, in my view, simply unsustainable.”

France has one of the lowest qualifying ages for a state pension among European countries and spends a significant amount supporting the system.

It is based on a “pay it forward” premise where younger workers, especially in the public sector such as education, transport or energy, pay higher than average taxes and earn lower wages but know they will be recompensed by leaving work while still relatively young and healthy, and live in comparable comfort, as a new generation will provide the public purse for them to do so.

There are exceptions in this system, such as farmers and agricultural workers who are classed as self-employed and generally in the private sector on private-owned farms. This means they may only qualify for a portion of any state pension, despite their importance to French society.

The pension programme is now facing financial challenges due to demographic changes — an ageing population and a significant fall in the birth rate — that burden the system’s finances.

France vs its neighbours

So, do French pensioners fare better than those in other developed economies? It depends on who you ask and what measure you use.

While the relatively early age of retirement can be envied, in terms of gross monthly payments the average monthly state pension in France at about 1,200 euros ($1,327) is significantly lower than many of its neighbours like Spain’s 2,500 euros ($2,764), Belgium’s 3,000 euros ($3,317) and Luxembourg’s 3,300 euros ($3,649). Two of them are also comparatively cheaper to live in, so against its literal neighbours, France’s retirement system does not seem so rosy.

However, with lower living costs than Nordic nations like Denmark, Norway and Iceland, and higher pension payouts than most of Eastern Europe, Ireland and the United Kingdom, France fares better than other parts of Europe. It is actually ranked seventh in the Breakeven Pension Index, a weighted table compiled by Almond Financial, a financial planning firm. In effect, French pensioners get a fairly healthy monthly sum and can live more cheaply than most other Europeans.

There is also a cultural dimension. Workers in France often see retirement as a genuine ‘third chapter’ in their lives rather than an afterthought, so they feel that leaving the workforce at a relatively young age is merited.

The system in numbers

French public sector employees typically receive higher pension benefits than those in the private sector and retire on average at 62.9 years of age, according to data from the European Commission, up to 2021.

The legal retirement age differs across Europe. In Germany, Italy and Denmark, it is 67, versus 66 in Spain (rising to 67 in 2027). In the UK, the current retirement age for a state pension is also 66, with Prime Minister Rishi Sunak hinting that he may push for raising it to 68.

On average, European Union inhabitants retire at 63.8 years, with Luxembourg having the lowest average retirement age, at 60.2 years.

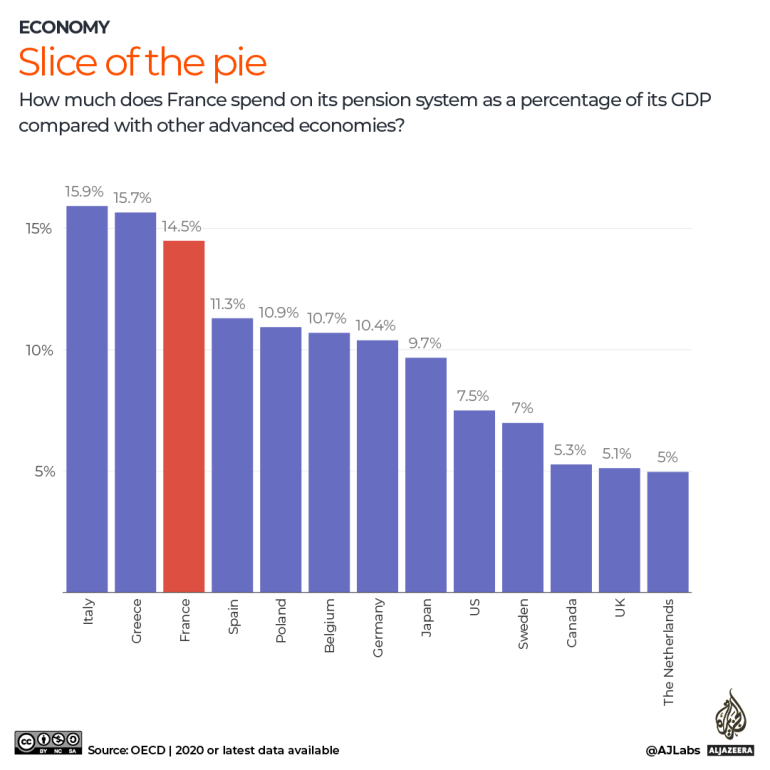

Then there is the amount that governments set aside for pensions.

According to the OECD, as a percentage of gross domestic product (GDP), France commits on average 14.8 percent to pensions. In the EU, only Greece (15.7 percent) and Italy (15.4 percent) shell out more. The European average is 11.6 percent with Poland devoting 10.6 percent of GDP to pensions, ahead of Germany at 10.3 percent and Romania at 8.1 percent, with Ireland coming last with 4.6 percent. The figure for the UK is 5.5 percent, according to London’s Office of Budget Responsibility.

“There is a strong cultural attachment to state provision of pensions and also to quality of life which the French rate highly in terms of years worked but also working hours per week, days of holiday per year, and so on,” Rainbow Murray, professor at Queen Mary University London’s School of International Relations, told Al Jazeera. “Retirement, at an age and level of finance where it can be enjoyed, is seen as a right.”

Liberté, Egalité … Réalité

However, perceptions of the French pension system come with caveats, says Paul Smith, associate professor in French History and Politics at Nottingham University.

“The generosity of the French system is something of a myth. Try being a farmer or in a profession that comes under the regime for farmers, for example,” he said, adding it is true that someone who qualifies for a full pension in France would receive about twice the level of support of, say, a UK pensioner receiving the full pension.

“But that’s because the French state takes a greater burden in terms of contributions and payout.”

However, the number of people who qualify for the full pension is far lower than you might think. A basic pension at 1,200 euros ($1,327) a month is something of a chimera.

“The problem is that many French people in fact live on a wage not very much higher than the minimum wage — teachers for example earn something like 1.5 times the minimum wage, so paying into a supplementary pension scheme is out of the question.”

Why such a violent response?

Despite Macron and his ministers claiming that they will give themselves “100 days of appeasement, unity, ambition and action” to heal the country, observers cannot help but feel a red line has been crossed.

“Macron has ripped up the relationship with trade unions and they do not seem likely to be willing to come to the table any time soon,” said Smith.

Added Barr: “Pensions are a device that allow younger people to plan over their life course and should be formed gradually with a long-term view. So sudden, sharp changes, especially for people close to retirement, is crazy design.”

But was this set of reforms a fundamental and necessary step to prevent a collapse of the system?

“Very much so”, said Barr. “Italy is a very sad illustration of ignoring the problem. Various governments kicked the can down the road for more than 30 years until the nasty stuff hit the fan, and then the Mario Monti administration in 2011 had to reform very radically and very quickly,” to avoid the country going bankrupt, he said.

[ad_2]

Source link