Imagine you woke up one day to discover your bank account has been raided by another country’s government. Just like that, $1 in every $16 of your supposedly safe money is gone. If you’re wealthy enough to have more savings, it could be $1 in $10. Is it a nightmare? The opening chapter of a Kafka story? A Bond villain plot to start a bank run and bring down the government?

Nah, it’s just the new reality facing bank depositors in Cyprus. And it might just set off a fresh wave of financial panic in the euro zone. Because we haven’t had enough of that lately.

Cyprus is the forgotten sick man of Europe. It’s so forgotten that it hasn’t even cracked the acronym of troubled European economies (the PIIGS or GIIPS, depending on your taste). But being forgotten has made it no less troubled. It needs money. And Germany isn’t exactly enthusiastic about handing over money, particularly in an election year for Chancellor Angela Merkel. Indeed, Germany has insisted on more than its usual pound of austerity in return for a bailout. It’s insisted that Cyprus pick up a large part of its own check. And that’s been terrible news for Cypriot savers. (And Russians. We’ll get there, soon.)

The terms of the Cypriot bailout (and bail-in) are as simple as they are startling. Germany will cough up about $13 billion, and, in exchange, Cyprus will levy a “one-time” tax on bank deposits to raise an additional $7.5 billion. This tax will take 6.75 percent from insured deposits of €100,000 ($129,000) or less, and 9.9 percent from uninsured amounts above €100,000. Depositors will get bank stock equal to whatever they lose from the tax. If you’re wondering why anybody would keep their money in a Cypriot bank now, well, they wouldn’t. This is an open invitation for an old-fashioned run on their banks. The only reason that isn’t happening now is their banks are closed for an extended holiday.

This bailout is the right answer to the wrong question. The wrong question is how Germany can bailout Cyprus (and a bunch of less-than-savory Russians) without risking Merkel’s reelection. The right question is how does Germany bailout Cyprus in a way that doesn’t risk the future of the euro at all.

Of course, there are all sorts of other questions here, all of them involving the word hell (or some other four-letter variation). Questions like: what the hell were they thinking, why the hell would Cyprus go along with this, and how the hell did an economy equal to 0.2 percent (!!!) of euro zone GDP become any kind of threat to the future of the euro? Well, as has often been the case, the answer begins with too big to fail, and in this case, too big to save, banks.

There’s Something Rotten in Cypriot Banks

There are four things you need to know about Cypriot banks. First, they have assets equal to roughly eight times the country’s GDP. Second, they get a huge percentage of their deposits from tax-dodging Russians. Third, they invested a ton of money in Greece. And fourth, they are highly dependent on central bank financing to stay afloat. In other words, Cypriot banks are too big for Cyprus to save. But somebody needs to save them.

How did all this money get into Cyprus banks? Like many other small islands, Cyprus has found that turning itself into a tax haven (and money-laundering center) is a pretty lucrative business. Money has poured in from Russian oligarchs and mobsters looking to avoid taxes back home, and that Russian money has bloated Cypriot banks to a size far beyond the government’s ability to bail out. Indeed, roughly 37 percent of the island’s €68 billion of deposits come from abroad — and as Kate Mackenzie of FT Alphaville points out, this foreign money makes up €25.5 billion of the €37.6 billion of deposits over €100,000. In other words, almost all of the foreign money is in uninsured accounts, and 68 percent of all uninsured accounts come from abroad.

So, what did Cyprus banks do with all of this money?Well, they invested it where they thought they had a competitive advantage: Greece. After all, southern Cyprus is ethnically Greek (the northern half is occupied by Turkey), and the Greek economy, which is 12 times larger than the Cypriot one, looked like an ideal place to expand. It wasn’t. Cypriot loans to the Greek government and businesses have opened black holes on bank balance sheets. In 2012 alone, two of the biggest Cypriot banks, Cyprus Popular and the Bank of Cyprus, lost a combined €3.5 billion on Greek bonds. That’s over 10 percent of GDP in a €31.8 billion Cypriot economy. It’d be like if Citigroup and JP Morgan lost $1.5 trillion in a single year (or approximately 250 times the “London Whale” losses).

The Cypriot banking system would have collapsed long ago were it not for emergency funding okayed by the European Central Bank (ECB). Here’s how it works. Suppose you run a euro bank desperately short on cash, collateral, and confidence. In other words, you need more money, but you so obviously need more money that nobody will lend it to you except on a secured basis — and only then against top-notch collateral, which you don’t have. Well, this is what lenders-of-last-resort are for, assuming your bank is illiquid and not insolvent. You can take your slightly crappy collateral to the ECB, and get a loan subject to a haircut. Technically-speaking, the worse your collateral, the higher the interest rate the ECB charges you.

But suppose your collateral isn’t just slightly crummy; say it’s really crummy. Well, don’t worry, you’re still in luck! The ECB won’t give you a loan, but your national central bank will, pending ECB approval. Welcome to the wonderful world of “emergency liquidity assistance” (ELA). Now, this sounds confusing (and that’s probably the intent behind it), but it’s really not. It’s the same idea as before, only with crappier collateral and higher interest rates. Remember, the ECB sets monetary policy for every euro member, but those members retain their own central banks, which carry out the ECB’s policy decisions. These national central banks can basically accept any collateral — really, anything — as long as they apply more severe haircuts and get the okay from the ECB. The only other big difference here is the national central banks, not the ECB, are on the hook in case of default.

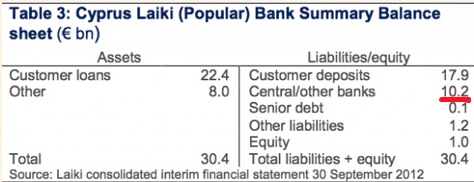

Cypriot banks have stayed alive by gorging on this ELA funding. The chart below from Joseph Cotterill of FT Alphaville shows the balance sheet of the second-biggest Cypriot bank, Laiki. Notice it gets a third of its capital from the central bank. That’s, um, a lot.

This dependence on central bank financing leaves Cyprus quite open to, shall we say, ECB persuasion. This, ladies and gentlemen, is what we call “foreshadowing”.

An Offer Cyprus Can’t Refuse — or Can’t Accept?

Cyprus needs €17 billion. Germany doesn’t want to give it €17 billion. Merkel doesn’t want to bail out Russian gangsters in an election year. So she’s forcing Cyprus to come up with €7 billion even though the government can’t afford it.

There are two ways a broke government could still come up with this money. First, it could force its own creditors or the banks’ creditors to take losses. But, as Joseph Cotterill points out, the Cypriot government can’t logistically force losses on its foreign lenders, and its domestic lenders are mostly its banks. In other words, the only losses the government can force on its bonds would make the banks’ problems all the worse.

That leaves the banks’ creditors. Most banks fund themselves with three classes of lenders: junior bondholders, unsecured senior bondholders, and secured senior bondholders, including insured depositors. If the bank goes bust, the secured senior bondholders are at the front of the line for whatever’s left, and so on. But Cypriot banks are almost entirely funded with deposits and ELA money. Now, junior bondholders did take €1.4 billion in losses, but there basically no unsecured senior bondholders. As Charles Forelle of the Wall Street Journal points out, the two biggest banks in Cyprus have €46 billion in deposits and €184 million in unsecured senior debt. In plain English, Cyprus has to make its depositors or its national central bank accept €5.8 billion in losses — and it can’t make its national central bank take losses.

So Germany is making Cypriot depositors pay. The questions are which depositors, and how much of their deposits. Cypriot president Nicos Anastasiades originally agreed to a 7 percent levy on deposit amounts above €100,000 and 3 percent below that, but the Germans decided that wasn’t enough, according to Peter Spiegel of the Financial Times. When Anastasiades tried to walk out in protest, ECB officials promptly informed him they would cut ELA funding for the second-biggest Cypriot bank, Laiki, if he didn’t agree. That would send Laiki into bankruptcy, and cost Cyprus €30 billion, versus the €5.8 billion the Germans wanted. It’s quite something when the ECB lets Germany use it as its debt collector. Of course, Anastasiades eventually acquiesced — though he insisted the top tax rate not exceed 10 percent, likely to preserve Cyprus’ future viability as a tax haven. That meant insured depositors had to be charged 6.75 percent to make the math add up.

It’s a total clusterf***. These tax rates still has to be approved by the Cypriot parliament, and, well, that’s not happening. The vote has already been postponed twice, and the Cypriots are back negotiating what they hope will be more politically acceptable tax rates. Under the latest plan, deposits under €100,00 would get 3 percent haircuts, deposit amounts between €100,000 and €500,000 would get 10 percent haircuts, and amounts over €500,000 would get 15 percent haircuts. This has the virtue of mostly hitting foreign depositors, and mostly sparing poorer, domestic ones. It should pass, but, then again, insured deposits shouldn’t be getting hit at all. Should is no guarantee.

Is the Euro Worth 5.8 Billion Euros?

The entire euro crisis comes down to a single question. Is a euro in a Spanish (or a Cypriot) bank worth the same as a euro in a German (or a Dutch) bank?

If Spain leaves the euro, then any euros in its banks will get turned into much cheaper pesetas overnight. Spanish depositors would be entirely rational to move their money to a German bank if they think there’s any chance Spain will abandon the common currency. Even a slow-motion bank run would only starve Spain of even more credit, and drag it down even further — making a euro exit all the more attractive. In other words, it’s a self-fulfilling fear.

Or at least it was, until ECB chief Mario Draghi stopped the vicious circle. Last July, he promised to do “whatever it takes” to save the euro — and those words alone were enough to end the panic. A Spanish euro was worth the same as a German euro once again. But what about a Cypriot euro? The tax on insured deposits resurrects the questions about whether a euro in a peripheral bank is worth the same as one in a core bank. It’s just due to fiscal risk now instead of exchange rate risk — but the effect is the same. Peripheral depositors would once again be rational to move their money. “One-off” events have a way of not always being so.

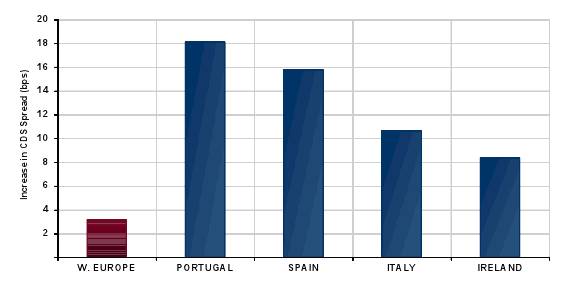

Now, that’s not to say that a continental bank run is looming. Credit default swaps on peripheral debt increased a bit relative to core debt as of 9:45 this morning, as you can see below in the chart from Bloomberg, but there’s no sign anything worse will happen. Markets have been mostly calm.

But just because there hasn’t been any contagion so far doesn’t mean it made sense to risk it over €5.8 billion. There’s nothing more destructive than giving people the idea that insured bank deposits are not so inviolable.

It’s a dangerous roll of the dice, for not much pay-off.