[ad_1]

Olaf Scholz came to power promising to alleviate Germany’s housing shortage by building 400,000 homes every year.

But nearly halfway through his term, the chancellor’s failure to reach that goal weighs heavily on millions of Germans struggling with high inflation, unemployment and rising rents.

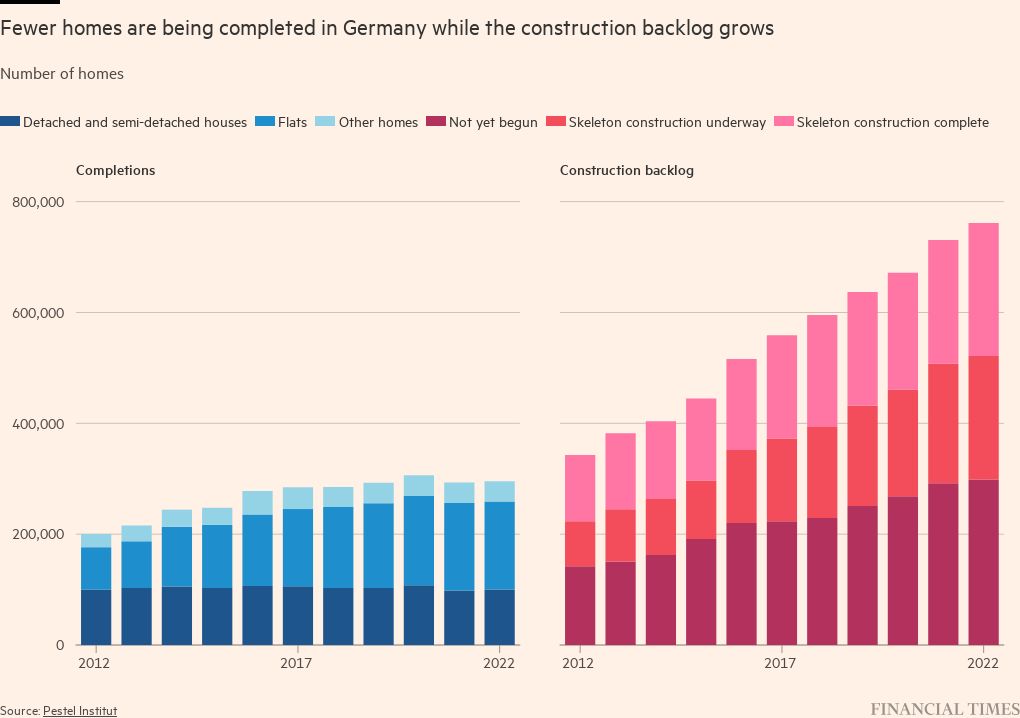

Just 295,300 dwellings were built in Germany in 2022, well short of the chancellor’s target. Industry executives expect the numbers for this year and next to be even lower — bad news in a country that is facing a shortage of 700,000 homes, according to the German Property Federation.

“The outlook for 2024-25 is catastrophic,” said Dirk Salewski, head of BFW, the German association of independent real estate and housing companies. “We are seeing a massive slump in demand for new developments.”

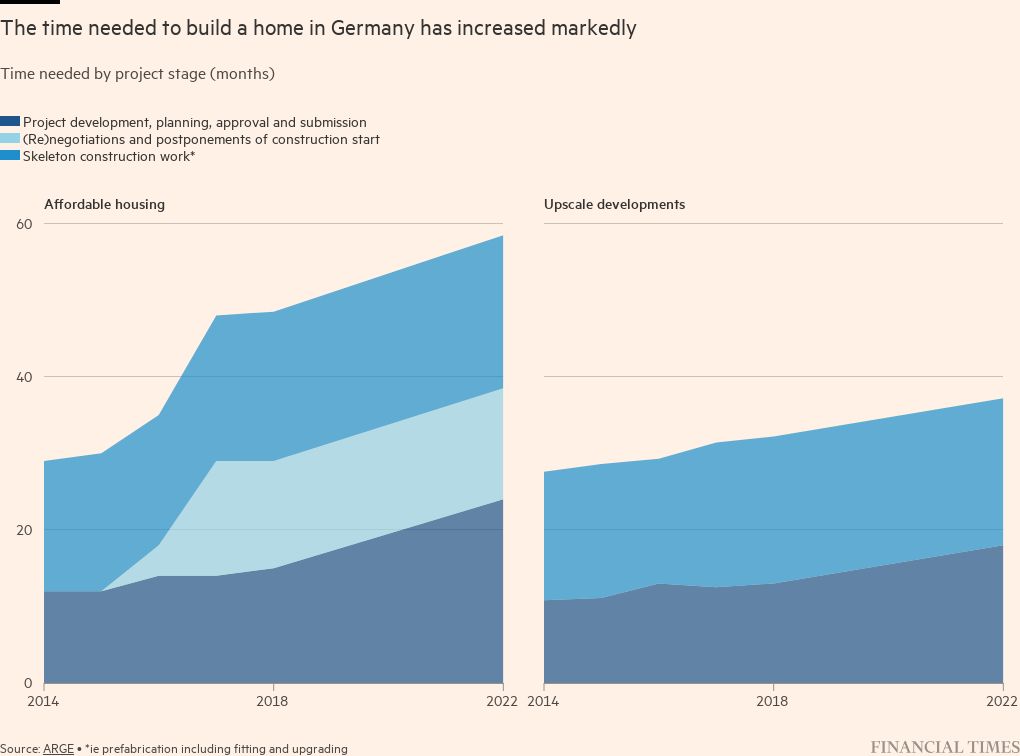

The industry is facing a perfect storm as interest rates and energy prices climb sharply, supply chain disruptions push up the cost of building materials and an acute shortage of skilled workers plays havoc with construction schedules.

The situation could deteriorate still. Building contractors have reported a sharp decline in orders — an alarming sign in a sector with long lead times. FIEC, Europe’s construction industry federation, said they fell 9.7 per cent in real terms in 2022, compared with the year before.

“Right now, building firms have full order books stretching into next year,” said Tim-Oliver Müller, head of HDB, the German construction industry association. “But there are no new orders coming in. And that is very worrying.”

The downturn could exacerbate an already overheated housing market where demand vastly outstrips supply. Empirica Regio, a research firm, has identified a “supply gap” of 23,177 dwellings in Berlin, 13,632 in Hamburg and 10,577 in Munich. In all three cities, rents are exploding.

Many contractors blame the government for the slowdown, saying it is imposing ever more burdensome environmental rules on developers, including a ban on new oil and gas-fired boilers, due to be adopted this year. They also criticise its decision last year to halt targeted support for new energy-efficient buildings.

The government insists it is taking steps to help the industry. It has launched a €2bn subsidy programme for “climate-friendly” construction, including €350mn a year in cheap loans for families on low incomes seeking to buy their own home. It is also providing €14.5bn in financial support for the building of social housing by 2026.

But experts say the subsidies — especially the cheap loans — will have little effect. “You only qualify if your house meets the highest energy-efficiency standards, and such houses are 20 per cent more expensive to build,” said Salewski. “How can people afford that?”

The upshot of the slowdown is clear, said Franz-Bernd Große-Wilde, chief executive of Spar- und Bauverein Dortmund, one of Germany’s oldest housing co-operatives. Decisions made today to shelve projects risk creating a substantial housing “gap” in two to three years. “It’s just going to become much harder for people to find a flat,” he said.

Established in 1893 to provide affordable housing for Dortmund’s industrial workers, the Spar- und Bauverein exemplifies the wider trend. For the first time in nearly 20 years, it has scrapped plans to build apartments.

“We’re taking a break from new projects,” said Große-Wilde. “With costs rising and fewer government grants on offer, you get less for every euro you invest.”

He said the company wouldn’t launch any more developments until all the others in planning have been executed. “That’s unusual compared to our approach over the last 15-20 years,” he said. Reflecting the move, its annual investment budget is to fall by €10mn to €40mn.

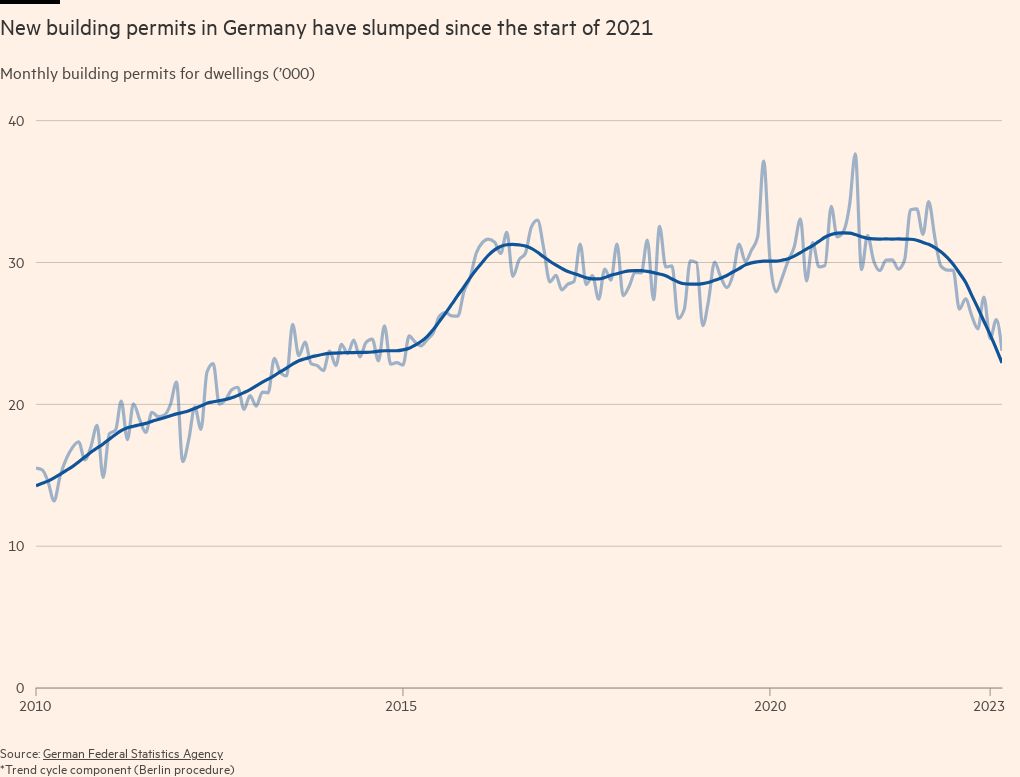

The company’s approach is typical for much of the industry. Investment in residential construction fell by 8.5 per cent to €9bn last year compared with 2021, while the number of building permits for new dwellings dropped by 27.3 per cent in the first four months of 2023, compared with the same period last year.

Residential completions are expected to fall from 295,300 in 2022 to 242,000 in 2023 and 214,000 in 2024, according to the GdW, a trade body representing housing associations. That compares with an annual average of 405,000 between 1950 and 2022.

Germany is not the only European country experiencing such headwinds. Building investment is expected to drop by 5 per cent in Spain and 5.7 per cent in Italy this year, according to FIEC. And France experienced a 15 per cent decline in housing starts and a 30 per cent fall in permits for new housing in the first four months of this year compared with the same period in 2022.

But the chill the sector is experiencing is particularly worrying in Germany, where the construction industry employs 2.5mn people, received €476bn in investment in 2022 and is a big driver of economic growth.

Concern about the state of the sector intensified in January when Vonovia, Germany’s largest property company, announced it was putting all its new building projects on ice.

Daniel Riedl, a member of Vonovia’s executive board, said it would have to charge rent of €20 a square metre in any new buildings to cover current construction costs of €5,000 a sq m — compared with €12 a sq m a couple of years ago. Yet such rents would, he added, be “completely unrealistic” for large parts of Germany, where the average rent is €7.5 a sq m.

Smaller companies, such as the BGFG building co-operative in Hamburg, are also slowing down their activities. It has shelved plans to construct 140 dwellings, the last stage of a large residential development on the Elbe River, south-east of Hamburg centre.

Peter Kay, BGFG’s chief executive, said the problem was not just higher material costs, but the fact that some materials had disappeared from the market completely. BGFG used to make its windows from Siberian larch, which has been banned under anti-Russia sanctions. “The alternative is oak and that is a lot more expensive,” he said.

Salewski of the BFW said the figure for completions last year was a “success” considering the effect of the war in Ukraine and its impact on supply chains. “The short- to medium-term outlook is a lot worse than the results for 2022.”

[ad_2]

Source link