[ad_1]

March 30, 2023 – Settlements are messy, especially those involving personal injury claims. Large and complex settlements require broad expertise involving the need to retain several different firms and organizations. The team assembled to administer the Gulf Coast Claims Facility to resolve claims from the widely reported BP oil spill, involved nearly a dozen professional services firms and several other specialty firms. “Independent Evaluation of the Gulf Coast Claims Facility Report of Findings & Observations,” BDO Consulting, Figure 1: Overview of the GCCF, GCCF Organizational Chart.

Careful consideration must be given up front to select the right mix of expertise to ensure a successful outcome. Each service provider must be evaluated against the specific requirements of the settlement program. This includes banks and financial institutions responsible for holding, investing, and distributing settlement proceeds.

Too often, financial institutions are selected based solely on general financial and banking metrics. In some cases, the selection of a bank or financial institution occurs absent a bid and proposal process. It is necessary for fiduciaries to establish a process to determine the appropriate financial structure and select the right financial institution(s) to avoid costly delays. Several fund specific factors must be considered to select the right institutions.

The following summarizes some key considerations applicable to most complex settlements when selecting banks and financial institutions. While each consideration is important, the critical question for special masters and fiduciaries is how well banks and financial institutions can accommodate uncertainty, which is inherent in most complex settlements.

Time is likely the first and most important factor. The anticipated length of a settlement program allows financial institutions to begin assessing risk and start developing a strategy. That said, the duration of most programs is at best an estimate. Even those with prescribed deadlines are often revised or delayed for a variety of reasons. Providing a range of potential scenarios when seeking a proposal helps evaluate flexibility and allows the financial institution to provide a variety of options.

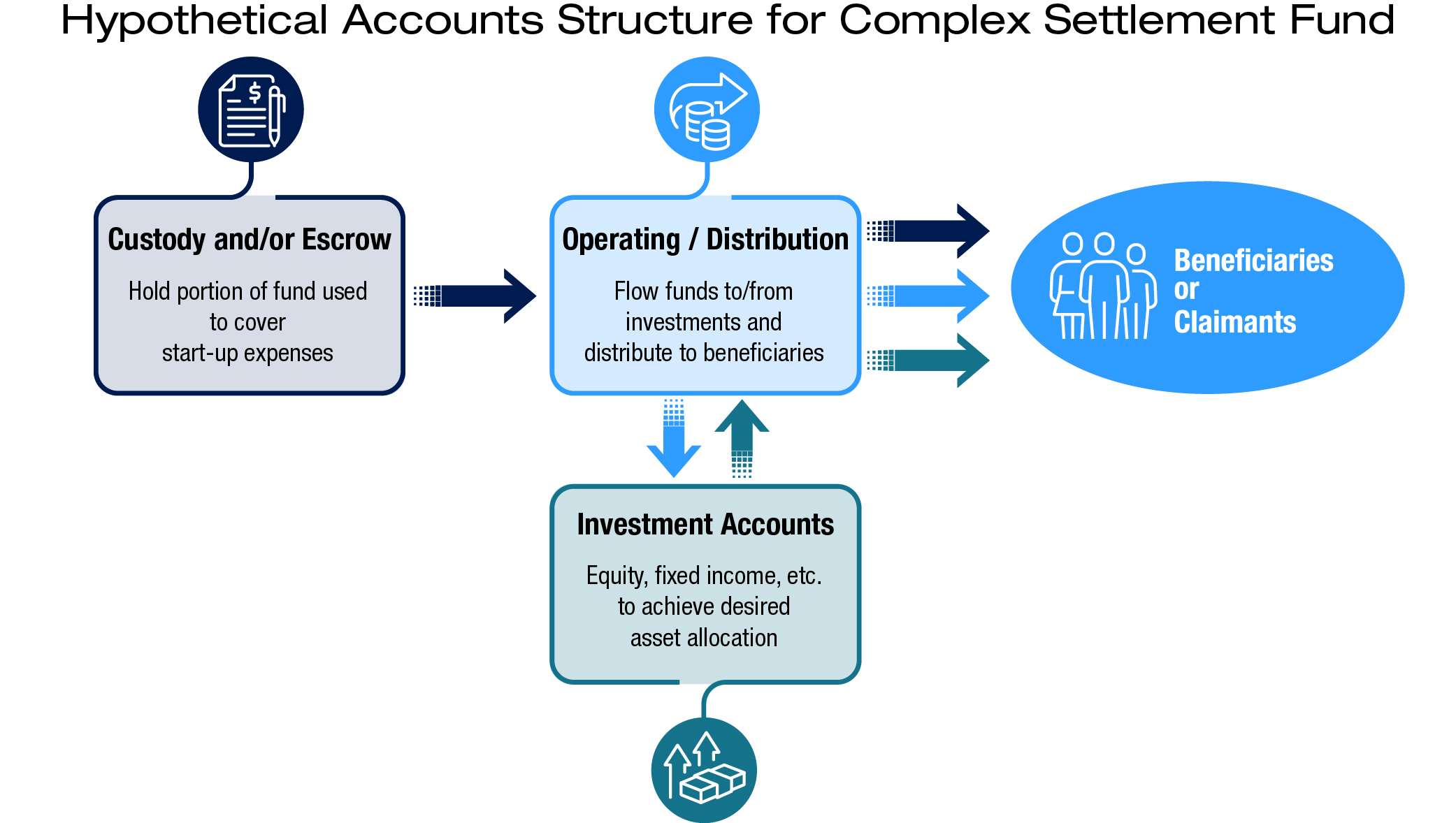

The size of the corpus, among other things, can play a critical role in whether to retain one or more financial institutions. The ideal structure may involve separate institutions for custody, investment, and distribution. Most major banks and financial institutions offer all these services under one roof. Having one institution provide all these services reduces complexity and can reduce costs. Generally, this structure is best for shorter term settlements where distributions are either scheduled or predictable.

On the other hand, it may be more prudent to spread funds across institutions or create a structure segregated by functions such as custody, investment, and distribution. The following illustrates a hypothetical structure that might be best used for a settlement with a large corpus and relatively long duration.

This structure requires more oversight. Transactions between institutions and accounts must be directed and authorized. The use of multiple entities reduces bank risk and can make it easier to replace institutions over time. This structure provides better protection and transparency but comes with added administrative costs.

The funds held by the settlements belong to the beneficiaries or claimants. Many settlements invest entirely in treasuries either directly or through money markets. Liquidity and asset preservation are more important than achieving aggressive returns, but diversification becomes important for longer term settlements with significant assets.

Determining liquidity needs requires a robust short- and long-term liability forecast. Cash requirements to pay claims should be continuously evaluated and balanced against the need to earn a reasonable return and preserve funds for future distributions. While a discussion about passive versus active investment management is well beyond the scope of this article, both have a place in the financial management of settlement funds and should be considered.

There are several events, common to most settlements, that can change the timing of future cash flows. These events can be either expected or unexpected. Expected events include filing deadlines, payout adjustments, additional notice requirements, future insurance installments, and specific wind down rules that are written into the settlement agreement or plan of reorganization. Unexpected events include recessions, bank failures, relevant scientific developments, catastrophic events, and political or economic shifts. All events should be appropriately modeled and considered when developing an asset allocation plan.

Most often, qualified settlement funds or “QSFs” are established to hold settlement funds. Many banks and financial institutions have experience with QSFs. However, most do not have experience with QSFs established for large and long-term personal injury settlements. QSFs are required to file a corporate form for income tax purposes, Form 1120-SF, where the “SF” stands for Settlement Fund.

It is critical for a bank or financial institution to recognize the QSF entity appropriately to allow for the reporting required to file corporate tax returns. In addition, investment managers must consider the long-term tax implications of the QSF entity and maximize the use of valuable tax assets such as net operating losses and net capital loss carry-forwards.

In conclusion, it is important to determine how familiar banks and financial institutions are with specific elements of settlement funds that influence investment and distribution activities. This is best achieved by developing a robust request for proposal that includes questions related to the considerations described here along with more general questions. The request should also include as much case-specific information as possible to solicit a comprehensive response.

Finally, fiduciaries should have an alternative plan or transition strategy in the event of an unforeseen event. As with all the considerations described above, the goal is to navigate uncertainty while expediting payments to beneficiaries or claimants.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias. Westlaw Today is owned by Thomson Reuters and operates independently of Reuters News.

[ad_2]

Source link