[ad_1]

The pillars of macroeconomic policy are fiscal policy and monetary policy with foreign exchange policy subsumed in the latter.

A disaggregation of these provides key variables that constitute an embodiment of the macroeconomic outlook; economic growth, employment, aggregate investment, general price level, interest rate, money supply, savings, taxes, public expenditure, public debt, exchange rate, and balance of payment position.

The stability or otherwise of these variables are reflective of the economic health of a polity and are certainly consequent on the decisions we make at the micro-levels – individuals, households, and firms.

These decisions are largely the byproducts of our propensities to consume, save, invest, import, and export.

They result from our cultural, political, and socio-economic consciousness of the present state of the economy and the capacities to drive same towards predetermined targets, but unfortunately, Nigerians carry on as if the state of the economy is devoid of our individual and collective actions and conveniently ‘push’ the blame to ‘others’.

In recent years the Nigerian economy has been characterized by instability. The exchange rate has tumbled, raising the degree of uncertainty in the foreign exchange market to an unprecedented level.

Before our eyes, we saw the US Dollar exchange for more than N1,300 in the parallel market and for slightly above N1,000 in the Official window.

The External Reserve of $33.23 billion reported in the Third Quarter of 2023 is not just the lowest the country has recorded in two years but is also incapable of sustaining the nation’s external commitments or obligations for seven months given the country’s annual import bill of $53.61 billion as at December 2022.

Public Debt stock (Domestic and External) has maintained its surge and devastating impact on the budgets and general public financial management strategy.

It has risen from N49.85 trillion in the first quarter of 2023 to N87.38 trillion in the second quarter, representing a growth rate of 75.27%.

Inflation has become a drunk variable. Its rise has been steep and continuous leaving a trail of its destructive impact on the value of money, wealth, and quality of life of the populace.

The latest report from the Bureau of Statistics put the indicator at 27.3 percent. The average Inter-Bank Call rate remains high at 24% while Monetary Policy Rate has been increased to 18.75%.

These are clear indications of inflation targeting monetary policy which is yet to yield a visible result.

In the same vein labour market indicators have sustained their rise without a wedge. The spirited surge of stock and flow variables of unemployment no longer makes news headlines even as the ‘workshops’ of idle minds and hands of the youth attain a catastrophic level.

Domestic saving is low thereby necessitating an inflow of foreign capital to augment the domestic capital accumulation. Interestingly, the reverse flow of this principal ingredient of production has gained currency with some highly reputed multinational corporations relocating offshores, including to our neighbouring countries.

This evidently shows that what the country attracts is basically ‘transit’ foreign capital. It may not be out of place to say that confusion beclouds strategic policy decisions to deal with the multifaceted macroeconomic crisis in the country.

High-interest rates, the complicated structure of taxes, high tax regimes, the rascality of the judiciary, the weak rule of law, the inordinate behaviour of the security operatives, corruption, the menace of revenue agents, and the sorry state socio-economic infrastructure have added fillip to the binding constraints of the cost of doing business in the country while limiting the production capacity of the economy.

Expectedly, the cumulative impact of the above scenario is an economy in dire stress as reflected in its primary fiscal target of economic growth.

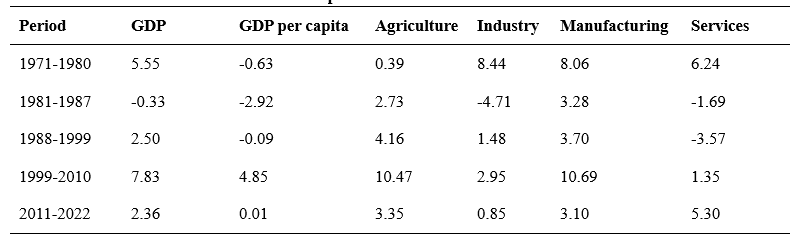

Computation done with data from different issues of the Central Bank of Nigeria Statistical Bulletin shows that although the goal of economic growth has been on the front burner of government policy the figure recorded since 1971 has not been quite impressive, especially for an economy that sees quantum leap in the volume of goods and services produced (Gross Domestic Product) as the be-all and end-all of macroeconomic policy.

An attempt has been made here to assess the economic growth performance of the economy under five periods; 1971-1980, 1981-1987, 1988-1999, 1999-2010, and 2011-2022.

As can be seen from the table below, the GDP growth rate has been erratic. It was 5.55% between 1971 and 1980 and declined to -0.33% for the period, 1981-1987 before rising with fluctuations to 2.36% between 2011 and 2022.

Of great interest here is that the substantial growth achieved between year 200 and 2011 was lost in the succeeding period of 2011-2022.

Similar trends are also observed in the sectoral composition of the GDP – Agriculture, Industry, Manufacturing, and Services.

Column 3 of the table captures the growth rates of per capita income for the five periods. It was negative for the first three periods which fall under 1971-1999.

It recovered from the sub-zero level to 4.85 between 2000 and 2010 before declining to almost zero between 2011 and 2022.

These figures speak volumes as they reflect the welfare level of the citizenry. In a nutshell, they simply say that the welfare of an average Nigerian has been on the decline since 1971 except the decade, 2000-2010.

Unfortunately, the lackluster response of the government to the deplorable condition of the average citizen has been sustained.

Periodic Growth rates of GDP and its composition

Source: Underlying data obtained from CBN Statistical Bulletin (various issues)

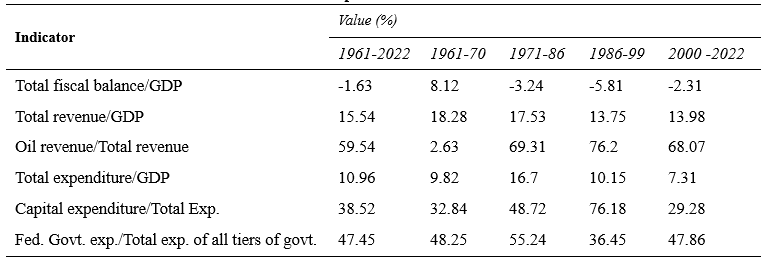

It also suffices to have a look at the fiscal indicators from the table below. The ratio of fiscal balance to the GDP has generally been stable and within a tolerable limit even as the ratio of revenue to GDP (relative fiscal capacity) captures the inability of the government to mobilise revenue that is commensurate with the size of the economy.

The ratio has stagnated around 14% even though expanded fiscal capacity was naturally supposed to be accompanied by increased size of the economy consequent of rebasing of same in 2014.

The domination of total revenue by oil revenue has become a permanent feature of Nigeria’s fiscal operation since 1971 with the ratio being above 71% is indicative of structural problems of revenue mobilization of the government especially concerning non-oil taxes.

Relative Size of Federal Government Fiscal Operations

Source: Underlying data obtained from CBN Statistical Bulletin (various issues)

It is also very glaring from this table that the ratio of capital expenditure to total expenditure of the federal government has been below 50% except for the period, 1986-1999 when it was 76.18%.

Worthy of note here is that this variable is below 30% between the years 2000 and 2022, the current dispensation of democratic governance.

This raises serious questions about the capacity of the government to grow and develop the economy. If capital formation cannot be deepened through increased capital expenditure, an incontrovertible fact is that the country will have to perpetually depend on capital imports to usher in the much-expected growth and development.

Another ugly picture from the above table is the dominance of the federal government in the total expenditure of the federation.

In fact, except for the period, 1986-1999 when the apex government accounted for only 36.45% of the total outlay of the country, the figure was generally above 48% thereby connoting stiffening of the fiscal operations of the lower-level governments whose revenue and expenditure actions are supposed to impact on the people directly.

The picture of Nigeria’s weak macroeconomy as seen above is unpalatable and fails to show the preparedness of an economy to be on a growth and development path.

These outcomes cannot be disassociated from poorly designed macroeconomic policy, weak implementation of those poorly designed policies, and general policy summersaults.

This has been the case even when different regimes of government unequivocally stated, time and again their commitment towards stabilizing the macroeconomic variables and repositioning the economy.

The deportment tendencies of the state, state agents, and institutions as derived from the philosophy of governance or absence of the same, the rule of law, and the response from the public determine macroeconomic behaviour.

The picture can only be different when the attitude and orientation of the government and the citizens on public policy matters change.

Written by

Isaac Chii Nwaogwugwu, PhD

The author is an Associate Professor of Economics at the University of Lagos

[ad_2]

Source link