[ad_1]

It sets the stage for a battle for business customers over the next 12 months. It is a critical segment for the major banks, since the returns from their home loan portfolios have been battered by the so-called “mortgage wars”.

UBS analyst John Storey said CBA’s business bank was more profitable than NAB and could be worth $69 billion on a stand-alone basis. There were more opportunities for CBA to grow the business bank by focusing on agribusiness and small business lending.

“Our research shows that CBA’s business banking segment could be a source of upside surprise to group earnings … possibly acting as a potential offset to some of the earnings pressure on retail from higher levels of competition,” Mr Storey told clients in a note on Tuesday.

Matthew Wilson, an analyst at Jefferies, said the banks had to make sure they had a more diversified revenue base as home loan lending slowed and mortgages remained competitive.

“This is a regime better suited to institutional/business banking where cashflow, capital and domain expertise matter. The sun might finally be setting on the industrialisation of asset-backed retail banking,” he said.

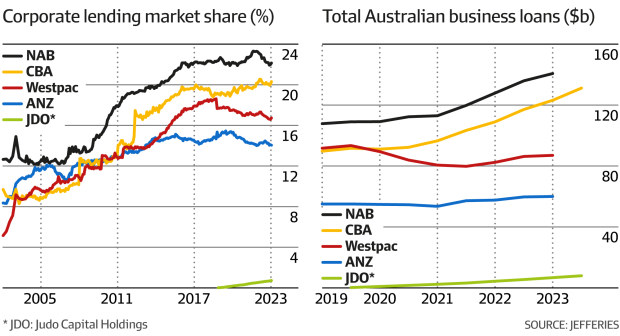

Mr Wilson said CBA had “done much better and gained share much faster in business banking” but believed it would be a challenge to knock off NAB as the largest lender in the sector. Aggressively chasing market share might not be in the best interest of the banks either, as some economists are fretting about a softer-than-expected GDP figure on Wednesday.

“A swing factor will be how the economy performs in the next 12-18 months. Winning share going into a traditional business cycle would probably drive some adverse [loan] selection,” Mr Wilson said.

“Business banking is almost the reverse of the mortgage market at the moment. CBA is letting a bit of market share go because Westpac is coming back to the market with low prices and cashbacks to win market share.”

Mr Irvine, NAB’s group executive for business and private banking, said the focus, for now, “is on helping our customers manage through what is a difficult time in Australia” as a study from Business NSW found that 23 per cent of companies are planning to cut jobs this quarter.

He does not believe that the bank’s bet on the healthcare industry would help keep competitors at bay because of the growth to come in the sector.

“Health is one of the areas that should be growing in excess of system for business credit overall. We have an ageing population, we have people living longer and illnesses are becoming more chronic,” Mr Irvine said.

“We are going to see patient care continuing to grow, and our goal is to continue to be the biggest in the space.”

Three weeks ago, CBA’s Mr Vacy-Lyle outlined the bank’s ambition.

Asked how long it would take for it to overtake NAB in terms of market share at the current pace of growth, Mr Vacy-Lyle said: “We have 26 per cent of the main bank market share, and you just optimise the insights you have and the relationships that you have, it is only a matter of time before you match your [business] lending share with your main bank share.”

“It is inevitability we will get there. But I don’t want to quote a particular date because I am going to be held to it by someone.”

[ad_2]

Source link