[ad_1]

NEW YORK, Oct 11 (Reuters) – Investors are primed for another period of strong U.S. profit growth as third-quarter reports from Corporate America flow in starting this week. But as business continues to emerge from the coronavirus pandemic, new problems are arising that are taking center stage for Wall Street, including supply-chain snags and inflationary pressures.

In the run-up to earnings season, a number of companies have issued downbeat outlooks. FedEx Corp (FDX.N) said labor shortages drove up wage rates and overtime spending, while Nike Inc (NKE.N) blamed a supply-chain crunch and soaring freight costs as it lowered its fiscal 2022 sales estimate and warned of holiday-season delays. read more

“The pace of growth is decelerating, but still it’s at a meaningful level,” said Terry Sandven, chief equity strategist at U.S. Bank Wealth Management. With the product and labor shortages and inflationary pressures, “we’ll be looking to see to what extent demand is there, and what does it mean for the important holiday spending period.”

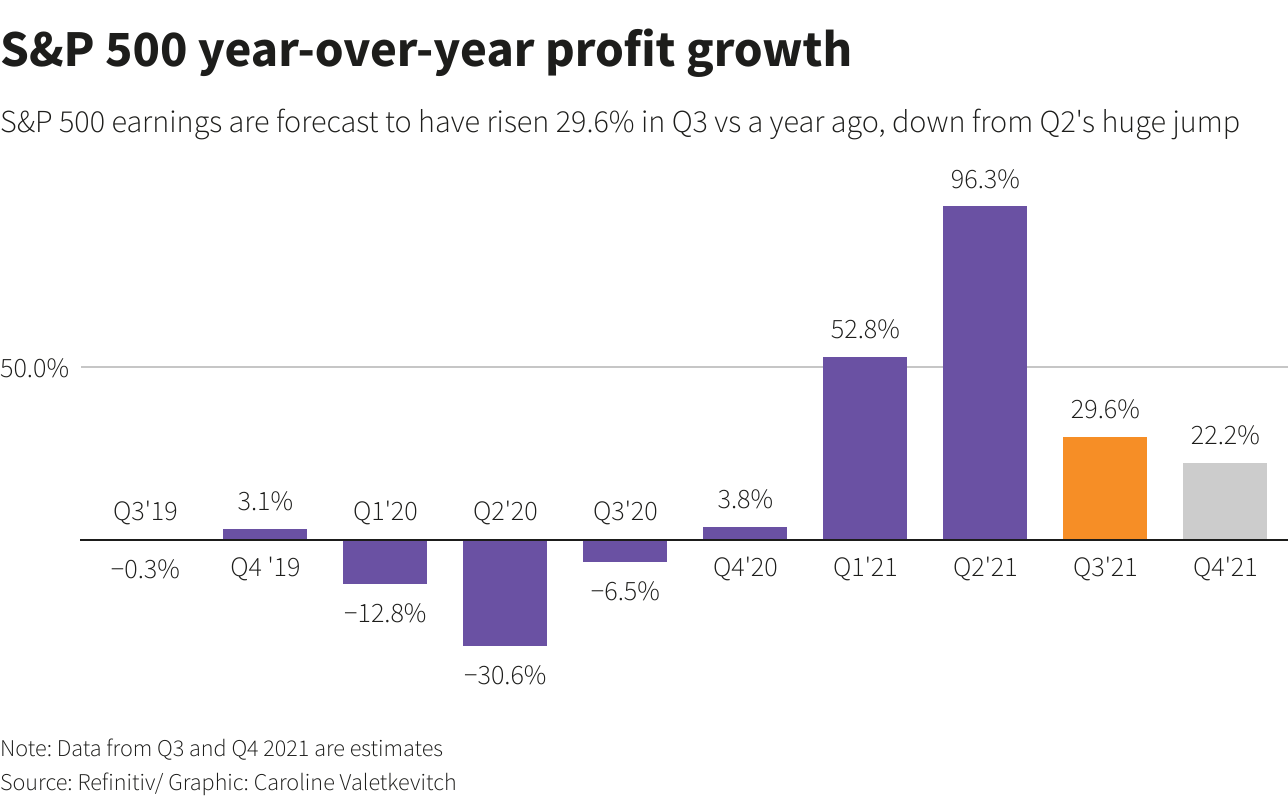

Analysts see a 29.6% year-over-year increase in earnings for S&P 500 companies in the third quarter, according to IBES data from Refinitiv as of Friday, down from 96.3% growth in the second quarter. The third-quarter forecast is down a touch from several weeks ago, a reversal of the recent trend for estimates.

Third-quarter earnings growth was always expected to be much lower than the blowout gain of the second quarter, when companies had much easier year-ago comparisons because of the pandemic.

“We were going up at such a high clip. The positive revision momentum has lapsed,” said Nick Raich, CEO of independent research firm The Earnings Scout.

Earnings season is kicking off this week with the big banks including JPMorgan Chase (JPM.N). read more

SUPPLY CHAINS, COSTS

Investors are weighing the impact of sharply higher energy costs on businesses and consumers after a recent surge in oil and natural gas prices. While higher energy prices should be a boon for energy producers, they are an inflationary risk for many other companies like airlines and other industrials and cut into consumer spending.

U.S. companies have so far this year kept profit margins at record levels because they have cut costs and passed along high prices to customers. Some investors are anxious to see how long that can go on. read more

Third-quarter earnings arrive with the market still wobbly after a weak and volatile September. The S&P 500 (.SPX) in September registered its biggest monthly percentage drop since the onset of the pandemic in March 2020. It was also the index’s first monthly decline since January.

Analysts are skeptical about how much is priced in.

“COVID-related supply chain issues have spread beyond consumer goods. And longer-term signs of global friction are easy to find,” Savita Subramanian, head of U.S. equity & quantitative strategy at BofA Securities, and other BofA strategists wrote in a note on Friday. These issues are far from being fully priced into stocks, they wrote.

Also, while supply chain issues have grabbed investor attention, wage inflation is “just as big of a headwind (if not bigger,” BofA strategists wrote in a note Monday. Guidance from companies “could be ugly,” they added.

Morgan Stanley’s analysts say that consensus earnings expectations also have not fully priced in the supply-chain constraints facing companies, making it much harder for companies to surpass estimates at the same rate as in recent quarters.

“Consumer Discretionary companies of all kinds are right in the cross hairs of the supply shortages, higher logistics costs and higher labor costs,” they wrote. Those strategists see the equity market set for a bigger pullback, and say third-quarter earnings could determine how deeply the stock market dips.

Reporting by Caroline Valetkevitch in New York

Editing by Megan Davies, Matthew Lewis and Richard Pullin

Our Standards: The Thomson Reuters Trust Principles.

[ad_2]

Source link